Arthur Hayes: Stablecoin IPOs Are a "Dead End", But I Advise Against Shorting

I'm not sure how Maelstrom will dance, but if there's money to be made, we'll go make it.

Original Title: Assume The Position

Original Author: Arthur Hayes, Crypto Trader Digest

Translation by: Bitpush

(Any opinions expressed here are the author's personal views and should not be considered as the basis for investment decisions, nor should they be interpreted as recommendations or advice for engaging in investment trading.)

Considering that Circle's CEO Jeremy Allaire seemingly had no choice but to assume the position under the “direction” of Coinbase's CEO Brian Armstrong (the author employs a sarcastic tone here, implying a lack of independence and control by Coinbase), I hope this piece will help those trading any “stablecoin”-related assets on public stock markets avoid significant risks and losses when promoters attempt to offload worthless assets onto unwitting retail investors. With that prelude, I’ll begin by discussing the past, present, and future of the stablecoin market.

In the realm of capital markets, professional cryptocurrency traders stand out as somewhat unique. For them to survive and thrive, they must have a deep understanding of how capital flows through the global fiat banking system. On the other hand, stock market investors or FX speculators don't need to understand the mechanisms of stock or currency settlement and transfer, as brokers handle these processes seamlessly in the background.

First of all, buying your first Bitcoin isn’t straightforward; determining the best and safest means to do so is not immediately clear. For many, the first step (at least when I entered the crypto space in 2013) involves purchasing Bitcoin by directly transferring fiat funds via bank wire or paying with physical cash to another person. Following this, you might graduate to trading on platforms offering bilateral markets, where you can transact larger volumes of Bitcoin at smaller fees. However, depositing your fiat funds into trading platforms is not or hasn't always been an easy or direct process. Many exchanges lack robust banking relationships or operate in regulatory grey zones within their jurisdictions, meaning users couldn’t wire funds to them directly. Exchanges devised workarounds, such as directing users to transfer fiat to local agents who would then issue cash vouchers on the platform or setting up adjacent businesses ostensibly unrelated to crypto to “normalize” their banking presence and enable fiat deposits under the radar of bank account managers.

Fraudsters have exploited this friction, stealing fiat funds in various ways. Exchanges themselves might misrepresent the whereabouts of user funds and one day… poof — the website disappears, along with the hard-earned fiat you deposited. If third-party intermediaries were used to move fiat in and out of crypto capital markets, these middlemen could vanish at any time, taking users’ money with them.

Since transferring fiat currency in the cryptocurrency capital markets carries inherent risks, traders must have a detailed understanding of and trust in the cash flow operations of their trading counterparts. When funds move through the banking systems of Hong Kong, mainland China, and Taiwan (regions I collectively refer to as Greater China), I learned how to navigate global payments.

Understanding how funds flow within Greater China helped me grasp how major Chinese-speaking regions and international trading platforms (like Bitfinex) operate. This is vital because all meaningful cryptocurrency capital market innovations originate from Greater China. This is especially true for stablecoins. Why does this matter? The reason will soon become obvious, so keep reading. The success story of the Western crypto world’s greatest trading platform belongs to Coinbase, which launched in 2012. Coinbase’s innovation lies in establishing and maintaining banking relationships in one of the world’s most adversarial markets toward financial innovation—the Pax Americana. Beyond that, Coinbase is simply a very expensive cryptocurrency brokerage account, which was sufficient to turn its early shareholders into billionaires.

I’m writing another lengthy piece about stablecoins because of Circle’s monumental IPO success. Let’s be clear: Circle is massively overvalued, but its stock price will continue to rise. This IPO marks the beginning, not the end, of the current stablecoin frenzy. After the public listing of a stablecoin issuer—likely on U.S. markets—the bubble will burst. The issuer will utilize financial engineering, leverage, and stunning performative skills to separate tens of billions of capital from fools. As always, most of those parting with their valuable capital will fail to understand the history of stablecoins and cryptocurrency payments, why the ecosystem evolved as it did, and what it means for which issuers will thrive. A very charismatic and credible person will take the stage, spout all sorts of nonsense, wave his (likely male) hands around, and convince you that the leveraged garbage he’s peddling is about to monopolize the multi-trillion-dollar total addressable market (TAM) for stablecoins.

If you stop reading here, the only question you need to ask yourself when evaluating an investment in a stablecoin issuer is this: how will they distribute their product? To achieve mass distribution—by which I mean the ability to reach millions of users at a reasonable cost—issuers must rely on the distribution channels of cryptocurrency exchanges, Web2 social media giants, or traditional banks. Without distribution channels, there is no chance of success. If you cannot easily verify whether an issuer has the ability to push its product via one or more of these channels, run for the hills!

Hopefully, my readers won’t burn their capital in this manner because, by reading this article, they’ll be empowered to think critically about the stablecoin investment opportunities presented to them. This article will discuss the evolution of stablecoin distribution. First, I will explain how and why Tether flourished in Greater China, laying the groundwork for its conquest of stablecoin payments in the Global South. Then, I’ll discuss the initial coin offering (ICO) boom and how it created genuine product-market fit for Tether. Next, I’ll delve into Web2 social media giants’ first foray into the stablecoin game. Lastly, I’ll briefly touch on how traditional banks might enter the space. To reiterate—because I know X (the platform) makes it hard to read prose that exceeds a few hundred characters—if a stablecoin issuer or tech provider cannot distribute products via cryptocurrency exchanges, Web2 social media giants, or traditional banks, they have no business entering this space.

Cryptocurrency Banking in Greater China

Currently, successful stablecoin issuers like Tether, Circle, and Ethena have the capability to distribute their products via major cryptocurrency exchanges. I will focus on the evolution of Tether and briefly touch upon Circle to illustrate why it’s almost impossible for new entrants to replicate their success.

In the early days, cryptocurrency trading was overlooked. For instance, from 2014 to the late 2010s, Bitfinex held the crown for the largest global exchange platform outside mainland China. At that time, Bitfinex was owned by a Hong Kong-based operations company, which maintained various local bank accounts. This was fantastic for arbitrage traders like me living in Hong Kong, as I could wire funds to the platform almost instantly. Right across the street from my apartment in Sai Ying Pun, there were nearly all the local banks, and I would walk between them carrying cash to minimize fees and the time it took to transfer money. This was crucial because it allowed me to turn over my capital once per day on weekdays.

Meanwhile, the three major exchanges of the time—OKCoin, Huobi, and BTC China—all maintained multiple bank accounts with large state-owned banks. A bus ride to Shenzhen took just 45 minutes, and armed with my passport and basic Mandarin skills, I opened various local bank accounts. As a trader operating in both mainland China and Hong Kong, having banking relationships meant you had access to all the liquidity globally. I also felt reassured knowing that my fiat wouldn’t disappear. In contrast, whenever I wired money to some Eastern European-registered exchange platforms, I lived in fear, as I didn’t trust their banking corridors.

However, as cryptocurrency gained visibility, banks started shutting down accounts. Every day, you had to check the status of each bank <> exchange relationship. This negatively impacted my trading profits, as the slower the funds moved between platforms, the less I could earn through arbitrage. But what if you could transfer electronic dollars on a crypto blockchain instead of relying on traditional banking routes? Then dollars—just as they were and still are today, the lifeblood of crypto capital markets—could move between exchanges 24/7 at almost no cost.

The team behind Tether collaborated with the original founders of Bitfinex to create such a product. In 2015, Bitfinex allowed the usage of Tether USD on its platform. At the time, Tether utilized the Omni Protocol as a layer on top of the Bitcoin blockchain to facilitate the transfer of Tether USD (USDT) between addresses. This was an early smart contract layer built on Bitcoin.

Tether allows certain entities to wire transfer USD to its bank accounts, in return, Tether mints USDT. USDT can then be sent to Bitfinex and used to purchase cryptocurrencies. Holy crap, that's freaking insane! Why would it be so exciting that some random trading platform offers this product?

Stablecoins, like all payment systems, only become valuable when a significant number of economically meaningful participants become nodes within the network. For Tether, besides Bitfinex, crypto traders and other major trading platforms must use USDT to solve any practical problems.

Everyone in Greater China is in the same boat. Banks are shutting down trader and platform accounts. Add to this, the fact that Asians want access to USD because their local currencies are prone to sharp devaluations, high inflation, and low domestic bank deposit rates. For most Chinese people, accessing dollars and U.S. financial markets is extremely challenging, if not outright impossible. So, a digital dollar version provided by Tether, accessible to anyone with an internet connection, has massive appeal.

The Bitfinex / Tether team seized the opportunity. Jean-Louis van der Velde, who has been the CEO of Bitfinex since 2013, previously worked for an automobile manufacturer in mainland China. He understands Greater China and has worked to make USDT the go-to crypto-friendly USD bank account for the Chinese-speaking community. While Bitfinex has never had a Chinese executive, it has built massive trust between Tether and the Chinese-speaking crypto trading community. Hence, you can be sure that Greater China trusts Tether. Meanwhile, in the Global South, overseas Chinese dominate the scene, just as imperial citizens found themselves navigating the unfortunate trade war, enabling Tether to serve as the de facto banking solution for the Global South.

Simply having one major trading platform as its initial distributor doesn’t guarantee Tether’s success. The market structure evolved to the point where trading altcoins against USD could only be done via USDT. Fast forward to 2017, at the peak of the ICO mania, Tether truly cemented its product-market fit.

ICO Baby

August 2015 was a pivotal month. The People's Bank of China (PBOC) triggered a shocking devaluation of the Chinese yuan against the U.S. dollar, and Ether (the native currency of the Ethereum network) began trading. Macro and micro shifts synced harmoniously. This was the stuff of legends and ultimately pushed the bull market that lasted until December 2017. Bitcoin skyrocketed from $135 to $20,000; Ether surged from $0.33 to $1,410. When the money printer starts rolling, macro conditions are always favorable. Since Chinese-speaking traders were the marginal buyers of all cryptocurrencies (at that time, this mostly meant Bitcoin), if they sensed instability in the yuan, Bitcoin would soar. At least, that was the narrative back then.

The shock devaluation by the People's Bank of China exacerbated capital flight. By August 2015, Bitcoin had plunged to $135 on Bitfinex—its lowest since Bitcoin's all-time high of $1,300 in February 2014, right before the Mt. Gox bankruptcy. Around that time, Zhao Dong (ZhaoDong), one of the largest OTC Bitcoin dealers in mainland China, faced the largest margin call in history on Bitfinex, amounting to 6,000 BTC. The narrative of mainland capital flight fueled a rally; from August to October 2015, BTCUSD more than doubled.

The micro is always the most fun part. The altcoin boom truly began with the launch of the Ethereum mainnet and its native currency, Ether, on July 30, 2015. Poloniex became the first platform to allow Ether trading. It was this foresight that vaulted it into the spotlight in 2017. Interestingly, Circle acquired Poloniex near the peak of the ICO bubble, only to stumble. Years later, they sold the platform at a massive loss to the illustrious His Excellency Justin Sun.

Poloniex and other Chinese-language trading platforms capitalized on the new altcoin market by launching crypto-only trading platforms. Unlike Bitfinex, these didn’t require integration with fiat banking systems. You could only deposit and withdraw cryptocurrencies to trade them for other cryptocurrencies. But this was less than ideal, as traders instinctively wanted to trade altcoin/USD pairs. Without fiat deposit and withdrawal capabilities, how could platforms like Poloniex and Yunbi offer these trading pairs? Enter USDT!

Following its release on the Ethereum mainnet, USDT could move across the network using the ERC-20 standard smart contract. Any platform supporting Ethereum could easily support USDT. As a result, crypto-only trading platforms could offer altcoin/USDT trading pairs to meet market demand. This also meant digital dollars could flow seamlessly between major exchanges—like Bitfinex, OKCoin, Huobi, and BTC China, where capital entered the ecosystem—and more niche, speculative venues, such as Poloniex and Yunbi, where gamblers played.

The ICO frenzy gave birth to the behemoth that is Binance. CZ (Changpeng Zhao) famously resigned as CTO of OKCoin following a personal dispute with its CEO, Star Xu. After departing, CZ founded Binance with the ambition of becoming the world's largest altcoin exchange. Binance had no bank account, and to this day, I’m unsure whether you can directly deposit fiat into Binance without going through certain payment processors. By leveraging USDT as its banking bridge, Binance quickly became the go-to platform for trading altcoins. The rest, as they say, is history.

From 2015 to 2017, Tether achieved product-market fit and built a moat to fend off future competitors. Due to the trust Tether garnered within the Chinese-speaking trading community, USDT was accepted across all major trading platforms. At this time, it wasn’t used for payments, but it became the most effective way to move digital dollars both into and within the cryptocurrency capital markets ecosystem.

By the late 2010s, trading platforms found it increasingly difficult to maintain bank accounts. Taiwan emerged as the de facto crypto banking hub for all the largest non-Western exchanges, which collectively controlled a significant portion of the global cryptocurrency trading liquidity. This was because several Taiwanese banks allowed these platforms to open USD accounts and somehow maintained correspondent banking relationships with major U.S. money center banks, like Wells Fargo. However, as these U.S. correspondent banks pressured Taiwanese banks to expel all cryptocurrency clients or risk losing access to the global USD clearing network, the arrangement began to deteriorate. Consequently, by the end of the 2010s, USDT became the only viable channel for large-scale USD transfers within the cryptocurrency capital markets. This solidified its position as the dominant stablecoin.

Western participants, many of whom raised funds under the narrative of enabling cryptocurrency payments, scrambled to create a competitor to Tether. The only one to survive at scale was Circle’s USDC. However, Circle operated at a significant disadvantage, being a U.S.-based company headquartered in Boston (ugh!) with no ties to the core of cryptocurrency trading and usage: Greater China. Circle’s implicit (and sometimes explicit) messaging, both past and present, was: Mainland China = scary; USA = safe. This messaging was comical given that Tether has never had ethnically Chinese executives, but it has always been associated with Northeast Asian markets in the past and, more recently, with the Global South.

Social Media Wants In

The stablecoin frenzy was nothing new. In 2019, Facebook (now Meta) decided it was time to launch its own stablecoin, Libra. Its appeal lay in Facebook’s ability to offer a dollar-denominated bank account to nearly everyone in the world outside Mainland China via Instagram and WhatsApp. Here’s what I wrote about Libra in June 2019:

The event horizon has passed. With Libra, Facebook has entered the digital asset industry. Before I begin my analysis, let me make one thing clear: Libra is neither decentralized nor censorship-resistant. Libra is not a cryptocurrency. Libra will destroy all stablecoins, but who the fuck cares. Not a single tear will be shed for all those projects that were somehow deemed valuable simply for being fiat-backed money market funds running on a blockchain, sponsored by no-name players.

Libra might bring about the decline of commercial banks and central banks. It could reduce their utility to that of a dumb, regulated digital fiat money warehouse—precisely what their role should be in the digital age. Stablecoins offered by Libra and other Web2 social media companies could have stolen the spotlight. These companies have the largest customer bases and virtually complete control over their preferences and behavioral data.

Ultimately, the U.S. political establishment stepped in to protect traditional banks from real competition in the payments and forex sectors. Back then, I commented on the matter: I hold no affection for the ridiculous remarks and actions of U.S. Congresswoman Maxine Waters during her time in the U.S. House Financial Services Committee. However, the panic displayed by her and other government officials wasn't driven by altruistic concerns for their constituents. Rather, it stemmed from a fear of disrupting the financial services industry—a sector that lines their pockets and helps maintain their positions of power. The speed with which government officials rushed to denounce Libra reveals that the project possessed some potential positive value for human society.

That was then. But now, the Trump administration seems poised to allow competition in financial markets. Trump 2.0 harbors no goodwill toward the banks that de-platformed his entire family during the Biden administration. As a result, social media companies are reviving plans to natively integrate stablecoin technology into their platforms.

For shareholders of social media companies, this is good news. These companies could fully absorb the revenue streams of traditional banking systems, payments, and forex markets. However, this spells bad news for any entrepreneurs looking to launch new stablecoins, as social media companies will build all the infrastructure they need to support their stablecoin businesses in-house. Investors in new stablecoin issuers must be wary of promoters boasting about collaborations or distribution deals with any social media company.

Other tech companies are also joining the stablecoin wave. Social media platform X, Airbnb, and Google are reportedly holding early-stage discussions about integrating stablecoins into their business operations. In May, Fortune Magazine reported that Mark Zuckerberg’s Meta—despite its previous failed attempts with blockchain technology—has been in talks with cryptocurrency firms to introduce stablecoins for payments. – Source: Fortune Magazine

My article “Libra: Zuck Me Gently”: https://blog.bitmex.com/libra-zuck-me-gently/

An Extinction-Level Event for Traditional Banks

Whether banks like it or not, they won't be able to continue raking in tens of billions of dollars per year merely for holding and transferring digital fiat. Nor will they earn the same fees for performing forex trades. I recently spoke with a board member of a major bank about stablecoins, and they said, “We’re doomed.” They perceive stablecoins as an unstoppable force, citing Nigeria as a case in point. I wasn’t previously aware of USDT’s penetration in that country, but they informed me that one-third of Nigeria’s GDP runs on USDT—even though the central bank has made serious efforts to ban cryptocurrencies.

```htmlThey continue to point out that because adoption is bottom-up rather than top-down, regulators are powerless to stop it. By the time regulators take notice and attempt to do something, it’s too late because adoption has already become widespread among the populace.

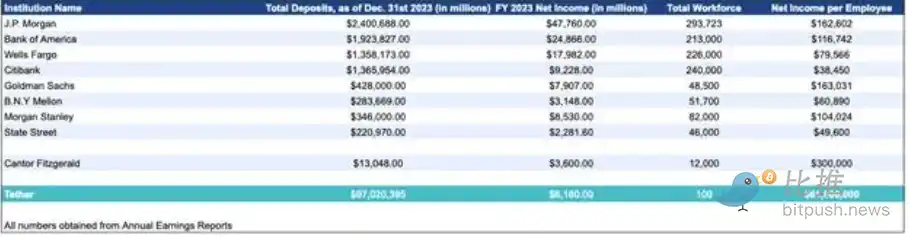

Although there are people like them at senior positions in every large traditional bank, the banking organism as a whole does not want to change because that would mean the death of many of its cells—its employees. Tether has fewer than 100 employees, yet it can leverage blockchain technology to perform the critical functions of the entire global banking system. For comparison, consider JPMorgan, arguably the best-run commercial bank in the world, which employs slightly over 300,000 people.

Banks are at a critical juncture—adapt or perish. However, complicating their efforts to streamline bloated workforces and provide products required by the global economy are prescriptive regulations about how many people must be hired to perform certain functions. As an example, let me recount my experience at BitMEX when trying to set up a Tokyo office and obtain a cryptocurrency trading license. The management team considered whether to open a local office and acquire a license to perform a few limited types of cryptocurrency trading activities outside our core derivatives business. The cost of compliance regulation was the issue, as you can’t leverage technology to meet the requirements. Regulators mandate that for each listed compliance and operational function, you must hire a person with an appropriate level of experience. I don’t remember the exact number, but I believe we needed approximately 60 people annually, each earning at least $80,000 per year, totaling $4.8 million annually to perform all mandated functions. All of this work could have been automated with a SaaS provider costing under $100,000 per year. And may I add, doing so would result in fewer errors than employing error-prone humans. Oh… and you can’t fire anyone in Japan unless you shut down the entire office. Yikes!

Banking regulations are essentially employment creation schemes designed for over-educated populations—a global problem. These individuals are over-educated in nonsense and not in what actually matters. They are merely well-paid box-tickers. While banking executives would love to slash their workforce by 99% and thereby improve efficiency, they can’t do so as a regulated entity.

Stablecoins will eventually be adopted by traditional banks, albeit in a limited capacity. They will run two parallel systems: the old, slow, and expensive system, and the new, fast, and inexpensive one. How much they are truly allowed to embrace stablecoins will be decided by the prudential regulators in each jurisdiction. Remember, JPMorgan is not a single organism but rather an instance of JPMorgan in each country, regulated differently. Data and personnel often cannot be shared across these instances, hampering firm-wide tech-driven rationalization. Good luck to you, you bastard bankers; regulation protected you from Web2, but it will ensure you meet your end in the Web3 era.

```These banks definitely won't collaborate with third parties for technological development or stablecoin distribution. They will handle all of these tasks internally. In fact, regulators may explicitly prohibit such cooperation. So, for entrepreneurs building their own stablecoin technologies, this distribution channel is essentially closed. I couldn’t care less about a particular issuer claiming to conduct a few Proofs of Concept for traditional banks. Such efforts will never lead to broad adoption within the banking industry. Therefore, if you're an investor and a stablecoin issuer promoter claims they will collaborate with traditional banks to bring their product to market, run—fast.

Now that you understand the challenges new entrants face in achieving large-scale distribution for their stablecoins, let’s discuss why they would attempt this impossible task anyway. Simply put, being a stablecoin issuer is extremely profitable.

The U.S. Dollar Interest Rate Game

The profitability of stablecoin issuers hinges on the amount of net interest margin (NIM) available. The issuer's cost base involves fees paid to holders, while their revenue comes from returns on cash invested either in government debt (like Tether and Circle) or certain crypto market arbitrage strategies (e.g., spot holding basis trades such as those used by Ethena). The most profitable issuer, Tether, doesn’t pay anything to USDT holders or depositors and earns the entirety of the NIM based on short-term Treasury bill (T-bill) yield levels.

Tether is able to retain its entire NIM because it has the strongest network effects and its customers have no alternative options for U.S. dollar banking services. Potential users don’t choose other dollar stablecoins because USDT is accepted across the global south. A personal example is how I make payments during the ski season in Argentina. I spend a few weeks skiing in the Argentinian countryside every year. Back in 2018, the first time I went to Argentina, payments were a hassle if vendors didn’t accept foreign credit cards. But by 2023, USDT had taken over—my guides, drivers, and chefs all accepted USDT as payment. It’s fantastic, because even if I wanted to, I couldn’t pay with pesos; ATMs in banks dispense at most $30 worth of pesos per transaction, accompanied by a 30% transaction fee. That’s outright criminal—so, long live Tether. For my staff, receiving digital dollars stored in a crypto exchange account or their mobile wallets, which they can easily use to purchase domestic and international goods and services, is wonderful.

Tether’s profitability serves as the best advertisement for social media companies and banks to create their own stablecoins. Both groups wouldn't have to pay for deposits because they already have rock-solid distribution networks, meaning they could capture the full NIM. As a result, this could become a massive profit center for them.

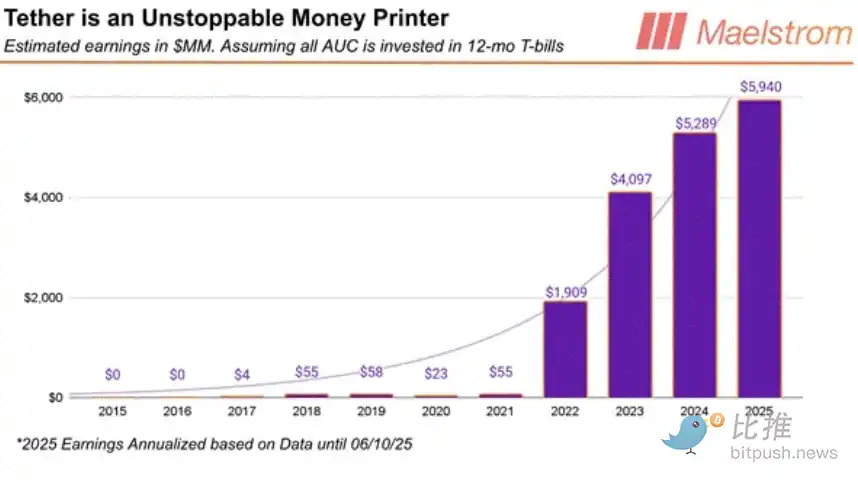

[Chart Description: Tether's Estimated Annual Revenue (in Billions USD) vs. Time (Years)]

Tether makes more money annually than this chart estimates. The chart assumes that all AUM (Assets Under Management) are invested in 12-month Treasury bills. The main takeaway is to show how Tether's earnings are highly correlated with U.S. interest rates. You can see the significant jump in revenue from 2021 to 2022, driven by the Federal Reserve hiking rates at the fastest pace since the early 1980s.

This is a chart I published in the article “Dust on Crust Part Deux,” and it makes it clear using 2023 data that Tether is the world's most profitable bank per capita.

Distributing stablecoins can be extremely expensive unless you're affiliated with an exclusive trading platform, a social media company, or a traditional bank. The founders of Bitfinex and Tether are the same group of people. Bitfinex has millions of customers, so right out of the gate, Tether had access to millions of users. Tether doesn’t have to pay for distribution because it is partially owned by Bitfinex, and nearly all altcoins trade against USDT.

Circle—and any other stablecoin issuer entering the space after it—must pay exchanges for distribution in one form or another. Social media companies and banks will never partner with third parties to build and operate their stablecoins; hence, crypto exchanges are the only option. Crypto exchanges could build their own stablecoins, as Binance tried with BUSD, but eventually, many exchanges find that building a payment network is too challenging and diverts attention from their core business. Exchanges require equity in the issuer or a share of the issuer’s NIM to allow trading of their stablecoins. But even then, all crypto/USD trading pairs are likely still matched against USDT, ensuring Tether continues to dominate the market. This is why Circle had to cozy up to Coinbase. Coinbase is the only major exchange not in Tether’s gravitational pull, as its users are primarily Americans and Western Europeans. Before U.S. Commerce Secretary Howard Lutnick endorsed Tether and provided banking services to it through his company Cantor Fitzgerald, Tether was heavily criticized in Western media as a purported foreign-made scam. Coinbase’s survival depends on the goodwill of U.S. political institutions, forcing it to find an alternative. Therefore, Jeremy Allaire “assumed the position” and accepted Brian Armstrong’s demands. [1]

The deal goes like this: Circle pays 50% of its net interest income to Coinbase in exchange for distribution across the entire Coinbase network. Yacht in hand (Yachtzee)!!

The situation for new stablecoin issuers is extremely tough. There are no open distribution channels. All major crypto trading platforms either own an issuer or have partnered with existing issuers like Tether, Circle, and Ethena. Social media companies and banks are building their own solutions. Therefore, a new issuer must relinquish a significant portion of its NIM to depositors in an attempt to pry them away from more widely adopted stablecoins. Ultimately, this is why, by the end of this cycle, investors will likely lose their shirts on nearly every publicly-listed stablecoin issuer or technology provider. But that won’t stop the party from raging on; let’s dive into why investors’ judgment is clouded by the massive profit potential of stablecoins.

Narrative

There are three business models responsible for creating crypto wealth beyond merely holding Bitcoin and other altcoins. These are mining, operating trading platforms, and issuing stablecoins. Take me, for example—my wealth stems from owning BitMEX, a derivatives trading platform, while the largest position and most absolute returns generated by Maelstrom, my family office, come from Ethena, the issuer of the USDE stablecoin. Ethena went from zero to becoming the third-largest stablecoin in less than a year in 2024.

The uniqueness of the stablecoin narrative lies in its appeal to traditional finance (TradFi) "squares," as it possesses the biggest and most obvious Total Addressable Market (TAM). Tether has already proven that an on-chain bank that simply holds people’s funds and allows them to transfer them back and forth can become the most profitable financial institution per capita in history. Tether achieved success despite a legal war (lawfare) waged against it by various levels of the U.S. government. Imagine what could happen if U.S. authorities were at least neutral toward stablecoins and allowed them some operational freedom to compete for deposits alongside traditional banks. The profit potential is insane.

Now consider the current setup: U.S. Treasury officials believe stablecoin AUC (Assets Under Custody) could grow to $2 trillion. They also believe that USD stablecoins could act as the spearhead for advancing or maintaining dollar hegemony while serving as buyers of U.S. Treasuries who are indifferent to debt prices. Whoa, that’s a major macro tailwind. As a delicious kicker, remember that Trump holds a grudge against big banks for de-platforming him and his family post his first presidential term. He has no intention of stopping the free market from offering better, faster, and safer mechanisms to hold and transfer digital dollars. Even his sons have jumped into the stablecoin game.

This is why investors are drooling over investable stablecoin projects. Before I continue with my predictions about how this narrative could translate into money-burning opportunities, let me first define the criteria for an investable project.

The issuer should be able to list in some form on a U.S. public stock market. Secondly, the issuer must offer a mobile digital dollar product; none of that foreign crap—this is ‘Murica. That’s it. As you can see, there’s a ton of room for creative maneuvering here.

The Road to Ruin

The most obvious issuer that might IPO and kick off the party is Circle. They are a U.S.-based company and the second-largest stablecoin issuer by AUC (Assets Under Custody). At this stage, Circle is heavily overvalued. Remember, Circle gives away 50% of its interest income to Coinbase. And yet, Circle's valuation is 39% that of Coinbase. Coinbase is a one-stop crypto financial shop with multiple profitable business lines and tens of millions of global customers. Circle, on the other hand, excels at fellatio—while this is a very useful skill, they still need to upskill and take care of their step-children.

Should you short Circle? Absolutely not! Perhaps, if you believe the Circle/Coinbase ratio is unbalanced, you should instead go long on Coinbase. Even though Circle is overvalued, years from now, when we look back at the stablecoin craze, many investors will wish they simply held onto Circle. At least they'd have some capital left.

The next wave of IPOs will be Circle copycats. Relatively speaking, these stocks will be even more overvalued in terms of price-to-AUC ratios than Circle. Absolutely speaking, they’ll never surpass Circle in earning potential. Promoters will tout meaningless traditional finance credentials, trying to convince investors they have the connections and ability to disrupt existing global dollar payment systems by working with or overtaking traditional banks. The scam will succeed; issuers will raise a ton of damn money. For those of us who’ve spent some time in the trenches, watching these suit-wearing clowns fool the public into investing in their junk companies is going to be hilariously ironic.

After this first wave, the scale of scams will depend entirely on the U.S. stablecoin regulatory framework. The more leeway issuers are given in terms of the assets backing their stablecoins and whether they can pay yields to holders, the greater the potential for financial engineering and leveraging to obscure the garbage beneath. If you assume light or hands-off stablecoin regulation, you might even witness a Terra/Luna-style event—a Ponzi scheme masquerading as an algorithmic stablecoin. Issuers could offer high yields to holders, with those yields generated by applying leverage to certain asset holdings.

As you can see, I don't have much to say about the future. There really is no future, because the distribution channels for new entrants have been shut down. Get that idea into your damn thick skull. Trade this piece of shit like a game of hot potato. But don’t short it. These new stocks will rip the faces off of shorts. Macro and micro are in sync. As Chuck Prince, the former CEO of Citigroup, famously said when asked about his company's involvement in subprime mortgage lending: "When the music stops, in terms of liquidity, things will get complicated. But as long as the music is playing, you've got to get up and dance. We’re still dancing."

I’m not sure how Maelstrom will dance, but if there’s money to be made, we’ll make it.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

CandyBomb x POWER: Trade to share 4,387,500 POWER

New users get a 100 USDT margin gift—Trade to earn up to 1888 USDT!

Bitget Spot Margin Announcement on Suspension of DOG/USDT, ORDER/USDT, BSV/USDT, STETH/USDT Margin Trading Services

BGB holders' Christmas and New Year carnival: Buy 1 BGB and win up to 2026 BGB!