Circle faces 'medium-term' risks from slow USDC growth, rising distribution costs: Mizuho

Quick Take Mizuho Securities equities researchers say Circle’s stock faces medium-term risks from slower-than-expected USDC growth, rising distribution costs, and a potential Fed rate cut. The analysts give a base case for CRCL of $84 and bear case of $40 through 2027, down from Wednesday’s closing price of $153.16 a day after the firm filed its quarterly earnings.

Circle Internet Group (ticker CRCL) closed down over 6% the day after posting a largely positive quarterly earnings report. The amount of USDC in circulation grew by 90% year-over-year to $61.3 billion, while the company’s total revenue and reserve income increased by 53% to $658 million.

And yet, Circle’s stock has started to "fade," according to Mizuho Securities equities researchers. The analysts see three possible reasons for the stock’s surprising underperformance.

Namely, there is a growing divide between USDC's “dreams” and “reality” of distribution. While the stablecoin saw 6% QTD growth amid rising interest in crypto, this falls short of the company’s outlook of achieving a long-term compound annual growth rate of 40%.

Couple this with growing distribution costs, “from 39% of the reserve pool in 2022 to 61% in 2024...and 64% in 2Q,” the analysts note, and Circle’s margins seem to be increasingly compressed.

This could be accelerated by rising competition following the introduction of the GENIUS Act. Already, several major institutions have signaled interest in launching or introducing stablecoins, and Circle’s biggest rival, Tether, is working on a reentry plan into U.S. markets.

Finally, the analysts say, while "cooling CPI is good news for the economy but bad news for CRCL." On Tuesday, the Labor Department reported that U.S. consumer prices rose 2.7% year over year in July, slightly below estimates, which raised some expectations that the Federal Reserve could cut interest rates.

"But this isn't good news for CRCL, which benefits from higher rates," Mizuho wrote Wednesday in a note to clients, explaining its base case for CRCL’s performance. "Given CRCL's dependence on a single macro factor (interest rates) and the potential for slower-than-expected USDC in circulation growth, we assign a market multiple to our below-consensus 2027E EBITDA to arrive at our PT of $84."

This is based on the fact that Circle's peer group, including Visa, Coinbase, and Robinhood, is currently trading around 23x EBITDA. A bear case accounts for slower-than-anticipated USDC growth of just 15% CAGR through 2027 to a $72 billion market cap, as well as lower interest rates to arrive at a price point of $40.

Of note, Bernstein analysts maintained a $230 price target on the stock.

Circle went public in June in a blockbuster IPO that saw shares rocket over 200% to over $90 per share on its first trading day. Shares are now trading hands at around $153.16 with a $41.1 billion market cap, according to The Block’s data .

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Crypto 2026 in the Eyes of a16z: These 17 Trends Will Reshape the Industry

Seventeen insights about the future summarized by several partners at a16z.

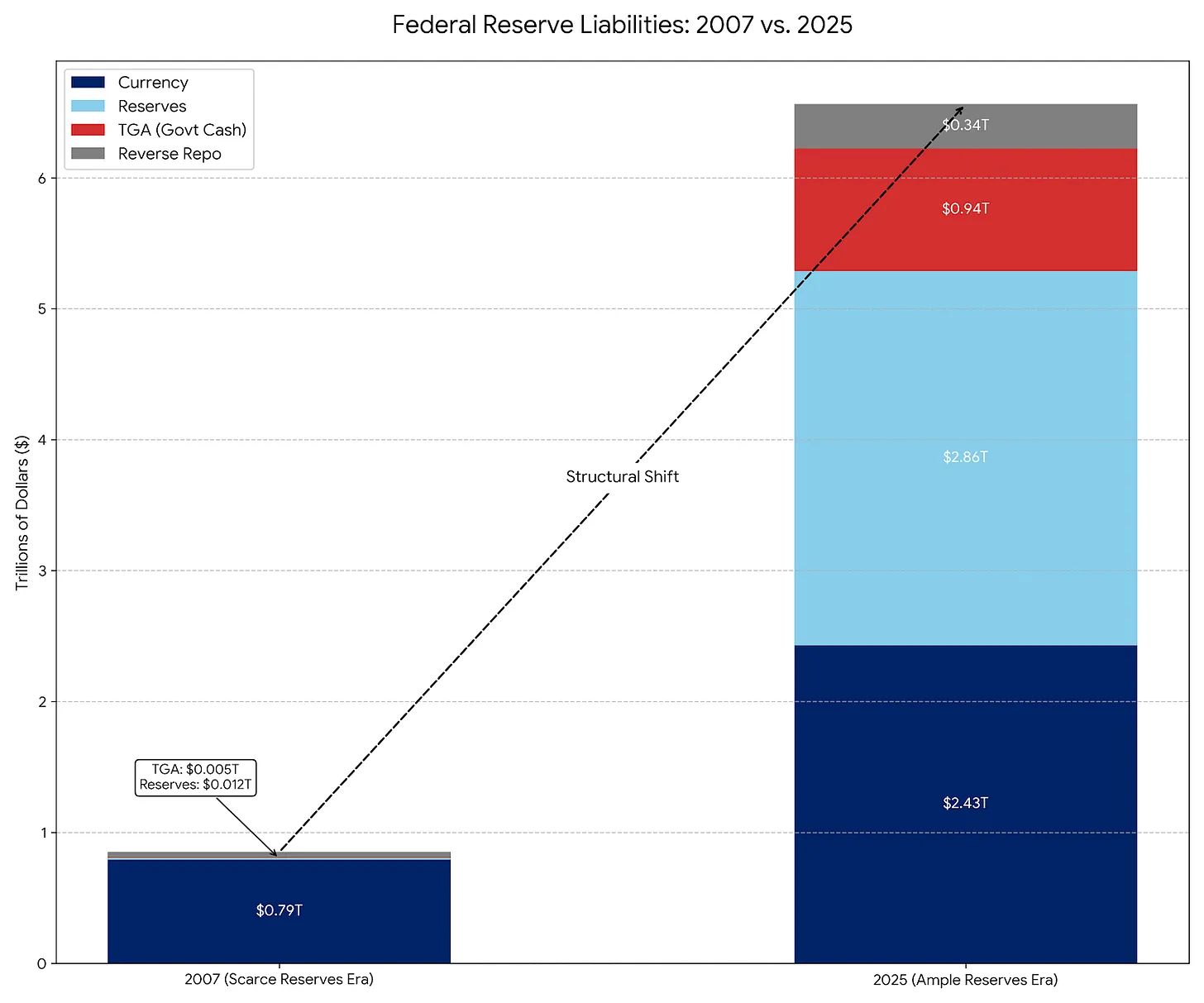

The Federal Reserve's $40 billion purchase of U.S. Treasuries is not the same as quantitative easing.

Why is RMP not equivalent to QE?

Tokenization of U.S. Assets: DTCC Gets Regulatory Green Light