Guotai Haitong Overseas: With the Federal Reserve restarting interest rate cuts, there is a possibility of foreign capital returning to Hong Kong stocks beyond expectations.

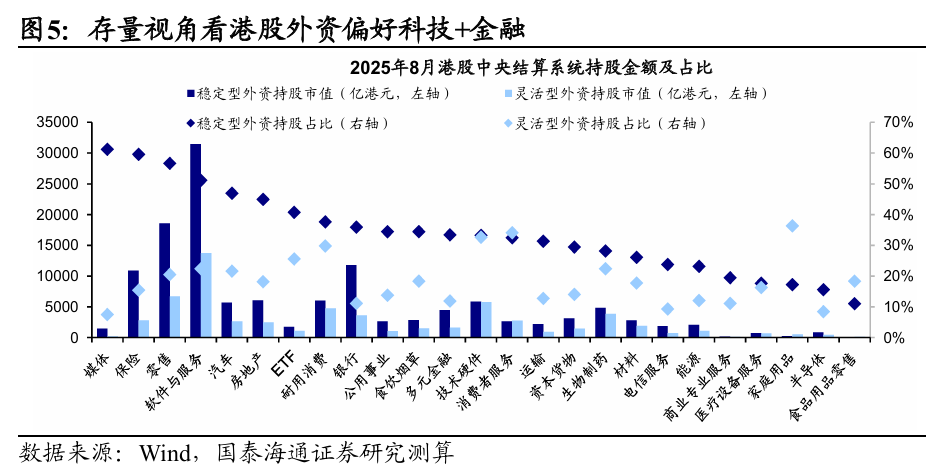

Guotai Haitong Overseas Strategy Team released a research report stating that since May this year, the China-US economic and trade negotiations have eased in stages, coupled with the continued fermentation of the weak US dollar logic, leading to a phased return of foreign capital to Hong Kong stocks. Looking ahead, the Federal Reserve's policy has clearly shifted recently, with Powell turning unexpectedly dovish at the annual meeting. The market currently expects the Federal Reserve to most likely restart the rate-cutting cycle in September this year, with two rate cuts expected within the year. The US dollar may continue to fluctuate in a weak pattern, and the subsequent stabilization of China-US trade relations is expected to provide a favorable macro environment for the marginal improvement or even an unexpected return of foreign capital, which is likely to continue the trend of foreign capital inflows since May.

From a stock perspective, the proportion of foreign capital holdings in Hong Kong stocks is high, with a preference for the technology and internet sectors representing China's new economic momentum, as well as the large financial sector relying on the national credit system. From a flow perspective, during 24/01-25/04, foreign capital largely flowed out of Hong Kong stocks, but there was a counter-trend inflow into some technology and consumer sectors, and since 25/05, there has been a consistent inflow into technology. As the negative factors suppressing Hong Kong technology stocks show positive changes, the low-valuation and fundamentally superior Hong Kong technology sector is expected to continue to attract foreign capital.

The main points of the report are as follows:

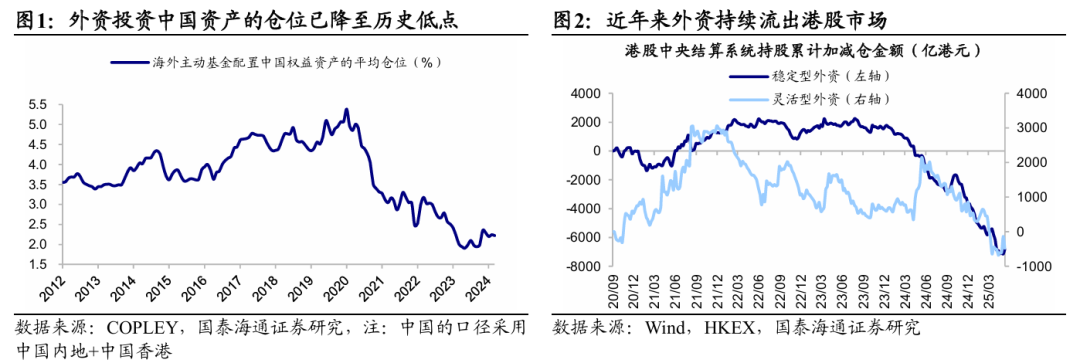

With the Federal Reserve restarting rate cuts, there is a possibility of an unexpected return of foreign capital to Hong Kong stocks. In recent years, affected by global geopolitical factors, foreign capital has cumulatively flowed out of the Hong Kong stock market by more than HKD 670 billions since September 2020, and the current allocation ratio of foreign capital to Chinese assets has reached a historical low. After several years of rapid outflows, foreign capital, which is more sensitive to geopolitical risks, may have already exited, and the current structure of existing foreign capital may gradually stabilize.

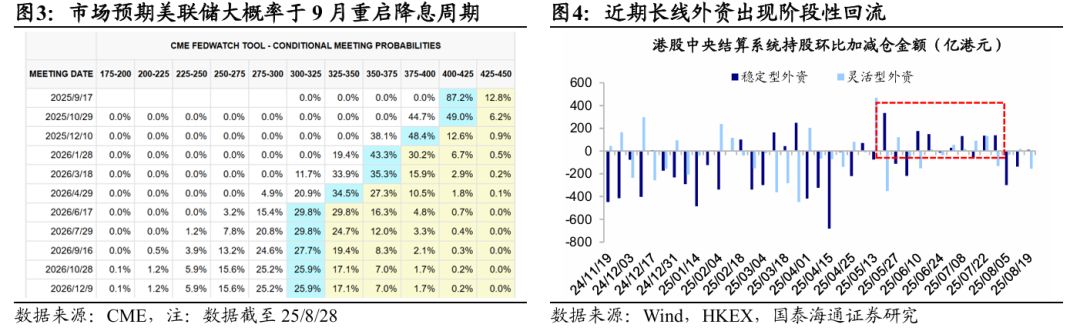

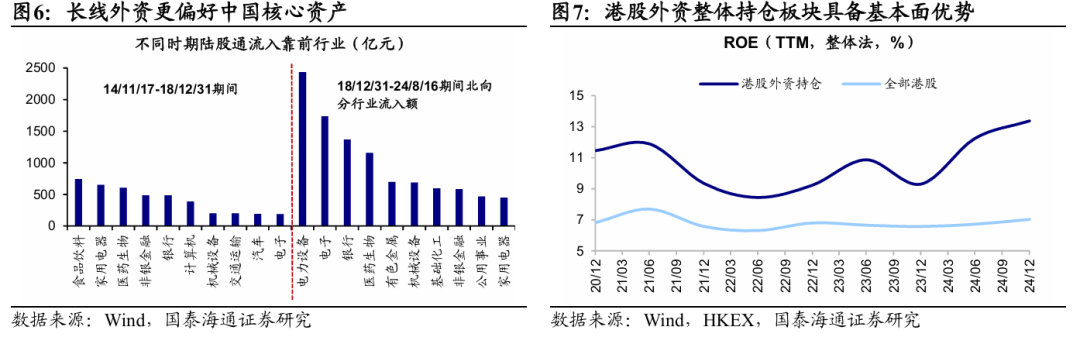

Since May, foreign capital has been returning to Hong Kong stocks. Since May this year, the China-US economic and trade negotiations have eased in stages, coupled with the continued fermentation of the weak US dollar logic, leading to a phased return of foreign capital to Hong Kong stocks. From May to the end of July, long-term stable foreign capital cumulatively flowed in about HKD 67.7 billions, and short-term flexible foreign capital flowed in about HKD 16.2 billions. At the beginning of August, as market attention to China-US trade negotiations heated up again, the previously returned foreign capital fluctuated again. As of 8/19, long-term foreign capital had cumulatively flowed out more than HKD 40 billions, and short-term foreign capital had flowed out about HKD 17 billions.

Looking ahead, the Federal Reserve's policy has clearly shifted recently, with Powell turning unexpectedly dovish at the annual meeting. The market currently expects the Federal Reserve to most likely restart the rate-cutting cycle in September this year, with two rate cuts expected within the year. The US dollar may continue to fluctuate in a weak pattern, and the subsequent stabilization of China-US trade relations is expected to provide a favorable macro environment for the marginal improvement or even an unexpected return of foreign capital, which is likely to continue the trend of foreign capital inflows since May.

The previous text mentioned signs of marginal stabilization and improvement of foreign capital recently. Coupled with the subsequent loosening of overseas liquidity, foreign capital is expected to become an unexpected variable affecting Hong Kong stocks within the year. The following will further analyze the preferences of foreign capital in Hong Kong stocks in recent years and recent changes.

From a stock perspective, foreign capital in Hong Kong stocks especially favors technology and finance. For a long time, foreign capital has dominated most sub-sectors of Hong Kong stocks, especially in the technology internet and large financial sectors. Specifically, as of 25/8/26, the sectors with the highest proportion of foreign capital in Hong Kong stocks are: retail (foreign capital overall 77%, of which long-term stable 57%, short-term flexible 20%, same below), insurance (75%, 60%, 15%), software and services (74%, 51%, 22%), media (69%, 61%, 7%).

Referring to the experiences of Taiwan and South Korea stock markets, as well as A-shares, foreign capital does not favor specific sectors, but rather regionally distinctive assets with fundamental advantages. The characteristics of foreign capital holdings in Hong Kong stocks also confirm this point: foreign capital prefers the technology internet sector representing China's new economic momentum, as well as the large financial sector relying on the national credit system. In addition, from the perspective of profitability, the preference of foreign capital holdings is also reflected. Since 2020, the median ROE (TTM, overall method) of Hong Kong stocks held by foreign capital is 10.7%, and the latest is 13.4%, significantly higher than all Hong Kong stocks at 6.8% and 7.0%, which also confirms that foreign capital prefers sectors with stronger profitability and fundamental advantages.

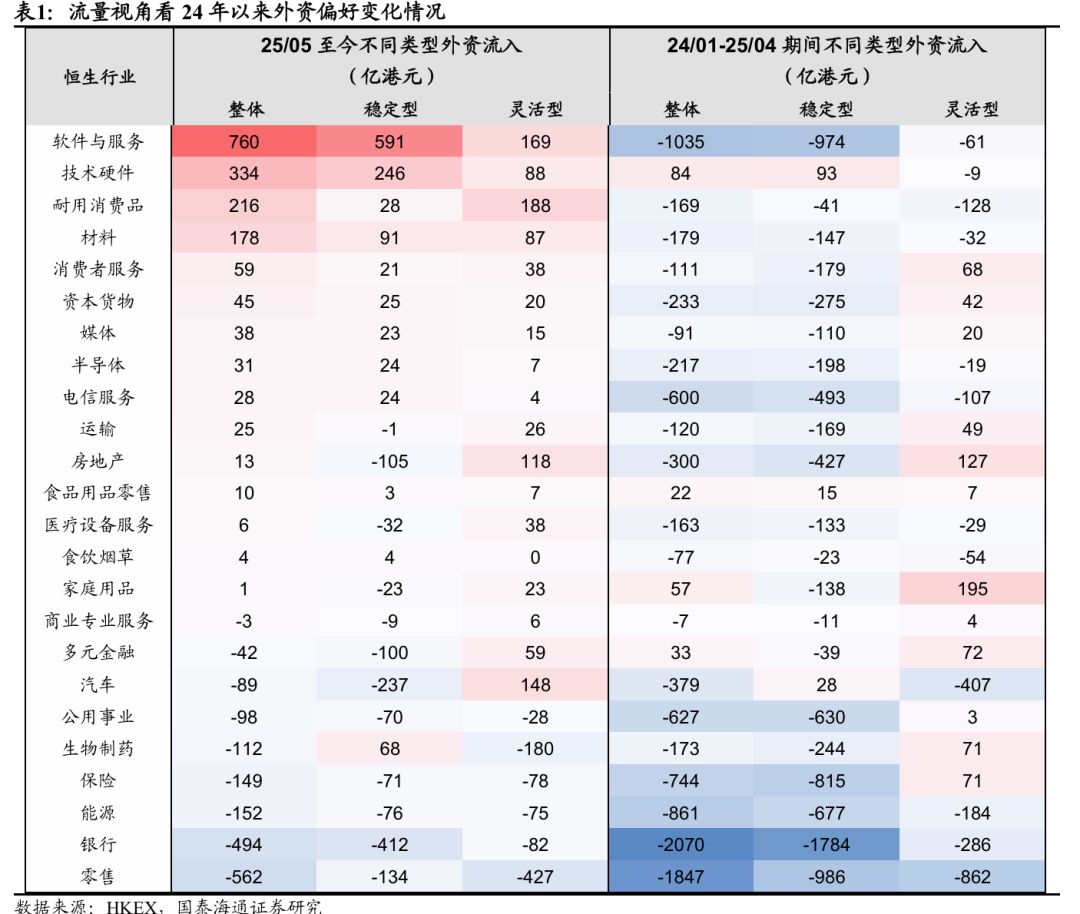

From a flow perspective, since 2024, foreign capital has counter-trend flowed into some technology and consumer sectors, and since May, has consistently flowed into technology. At the beginning of 2024, Hong Kong stocks rebounded from the bottom, but foreign capital continued its trend of outflows until signs of improvement appeared in May this year. Therefore, the foreign capital flow situation during 24/01-25/04 and since 25/05 was examined separately. During 24/01-25/04, foreign capital increased positions in hardware (cumulative inflow of HKD 8.4 billions, of which long-term stable HKD 9.3 billions, short-term flexible -HKD 0.9 billions, same below) and food products (HKD 2.2 billions, HKD 1.5 billions, HKD 0.7 billions).

As for the outflow sectors, most industries faced selling pressure, with the leading outflow sectors being banks (-HKD 206.7 billions, -HKD 178.4 billions, -HKD 28.6 billions), retail (-HKD 184.7 billions, -HKD 98.6 billions, -HKD 86.2 billions), and software services (-HKD 103.5 billions, -HKD 97.4 billions, -HKD 6.1 billions). Overall, during 24/01-25/05, foreign capital increased positions in technology and consumer sub-sectors, and significantly reduced holdings in large financial and technology internet sectors with high holding ratios, possibly due to foreign capital reducing exposure to heavily held sectors in consideration of geopolitical and other factors.

Looking at recent foreign capital trends, since May, both long- and short-term foreign capital have consistently flowed into software, hardware, and other technology sectors, while there are divergences in real estate and pharmaceuticals, and consistent outflows from dividend and retail sectors. Specifically:

① Consistently inflowed sectors: Since May, long- and short-term foreign capital mainly returned to technology sectors, with software and services (since 25/05, cumulative foreign capital inflow of HKD 76 billions, of which long-term stable inflow of HKD 59.1 billions, short-term flexible inflow of HKD 16.9 billions, same below), and technology hardware (HKD 33.4 billions, HKD 24.6 billions, HKD 8.8 billions) leading the inflows. This may be due to the accelerated iteration of AI technology represented by DeepSeek, coupled with industrial policy support, foreign capital's consensus on the currently undervalued Hong Kong technology sector is strengthening. In addition, durable consumer goods (HKD 21.6 billions, HKD 2.8 billions, HKD 18.8 billions), materials (HKD 17.8 billions, HKD 9.1 billions, HKD 8.7 billions), and other sectors have also seen significant inflows from both long- and short-term foreign capital.

② Sectors with divergence between long- and short-term: The sectors with the greatest divergence are mainly in biopharmaceuticals, real estate, and automobiles. Among them, biopharmaceuticals (-HKD 11.2 billions, HKD 6.8 billions, -HKD 18 billions) are still being increased by long-term funds, but short-term funds are clearly flowing out. This may be because funds are still optimistic about the fundamentals of innovative drugs, but since the innovative drug market has risen considerably this year, short-term funds tend to take profits in stages. In addition, automobiles (-HKD 8.9 billions, -HKD 23.7 billions, HKD 14.8 billions), real estate (HKD 1.3 billions, -HKD 10.5 billions, HKD 11.8 billions), and other industries have seen more short-term flexible foreign capital buying recently due to short-term policy or event catalysts, but long-term foreign capital is still in an outflow trend.

③ Consistently reduced sectors: Both types of foreign capital have jointly flowed out of banks (-HKD 49.4 billions, -HKD 41.2 billions, -HKD 8.2 billions), energy (-HKD 15.2 billions, -HKD 7.6 billions, -HKD 7.5 billions), utilities (-HKD 9.8 billions, -HKD 7 billions, -HKD 2.8 billions), and other dividend assets. At the same time, affected by the negative impact of the food delivery war on profitability, the retail sector has also been significantly reduced by both long- and short-term foreign capital (-HKD 56.2 billions, -HKD 13.4 billions, -HKD 42.7 billions).

The low-valuation and fundamentally superior Hong Kong technology sector is expected to continue to attract foreign capital. Currently, the valuation of the Hong Kong technology sector is not high, with the Hang Seng Technology PE (TTM) at the 18th percentile since 2020. As AI leads the technology cycle upward, the leading Hong Kong technology stocks with scarcity may have greater upside potential. Since the second quarter, the Hong Kong technology sector has performed weakly and fluctuated, mainly due to internet capital expenditures falling short of expectations and the negative impact of the "food delivery war" on the profitability of some internet platform companies. Recently, this suppressing factor may have improved: first, with the marginal easing of China-US trade, technology export controls have loosened; second, the impact of the "food delivery war" on internet companies may be nearing its end. This week, the National Development and Reform Commission and other departments drafted the "Internet Platform Price Behavior Rules" to regulate price competition on internet platforms.

Recently, the funding situation for Hong Kong technology stocks has shown positive changes, with both long- and short-term foreign capital consistently flowing into the Hong Kong technology sector. Looking ahead, Hong Kong technology leaders are widely distributed in the AI industry. As the AI industry trend is further confirmed, Hong Kong technology leaders will fully benefit from the AI industry transformation dividend, and their upward elasticity may be even greater.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Courts Crack Down on Digital Wealth Evasion with PIX and Crypto Seizures

- Brazilian courts freeze PIX keys and seize crypto from wealthy debtors to enforce financial obligations. - Measures target digital asset evasion, expanding judicial tools to track decentralized cryptocurrencies and payment systems. - AI-driven compliance tools now support real-time monitoring of suspicious transactions in Brazil's anti-money laundering efforts. - Global precedent emerges as courts demonstrate ability to regulate digital wealth, challenging traditional notions of financial privacy.

Institutional Capital Goes Onchain: Tokenized Assets Redefine VC Investment

- VC industry transforms via tokenized real-world assets (RWAs), driven by market maturation and investor demand shifts. - Institutional alternative funds (IAFs) surged 47% to $1.74B, with Ethereum dominating 50% TVL in tokenized assets. - Centrifuge (40.4%) and Securitize (37.5%) lead RWA platforms, enabling faster settlements and institutional blockchain adoption. - Aave's Horizon platform unlocks stablecoin liquidity for tokenized assets, while Chainlink ensures compliance via smart data tools. - Tokeni

XRP News Today: XRP's Future Hangs on Liquidity Battle With Tech Giants

- Ripple launches "Ripple Payments" demo to highlight XRP's role as a liquidity bridge for cross-border transactions, targeting banks seeking streamlined solutions. - Google's Cloud Universal Ledger (GCUL) emerges as a competitive alternative, offering multi-asset settlements via a single API, potentially reducing XRP's demand as a bridge currency. - XRP's price fell below $2.90 amid a 22.5% decline since July 18, with analysts predicting further downward movement before a potential Wave 5 recovery to $2.6

WIN -5.88% on 12-Month Slide Amid Volatile 7-Day Surge

- WIN’s 1-year price drop of 4,478.25% highlights extreme volatility and a severe long-term bearish trend. - Despite a 38.72% 7-day surge, the asset remains in a steep 507.32% monthly decline, underscoring structural instability. - Mixed technical indicators show short-term strength but overwhelming bearishness in longer-term trends, driven by regulatory risks and liquidity issues.