Letter from the Founder of Figure, the First RWA Stock: DeFi Will Eventually Become the Mainstream Method for Asset Financing

IPO is just one step in the long process of bringing blockchain into various aspects of the capital market.

Original author: Mike Cagney, Founder of Figure

Original source: Pantera Capital

Translated by: Zhou, ChainCatcher

Blockchain lending company Figure went public on September 11 and was listed on the US stock market. On its first day of trading, the stock price rose as much as 44%, with a market capitalization of about $7.8 billions; at the close, the total market cap was $6.5 billions.

This article is an open letter from Figure founder Mike Cagney regarding the IPO:

At the end of 2017, I had my "aha" moment with blockchain. When I was CEO at SoFi, I would often make statements about bitcoin and, more broadly, blockchain—"It will change financial services!"—but I didn't really know how it would change things. This time, it was different.

If you ask any full-stack engineer, most will say they'd rather not develop on blockchain: it's slow, cumbersome, and due to its immutable nature, has very low fault tolerance. But blockchain has a superpower—it replaces trust with truth.

Financial services have always been, and still are, trust-based markets. Such markets require a large number of intermediaries: between a public stock trade, there can be up to seven middlemen; even a debit card transaction may involve five participants. Many companies with huge market caps are built around this kind of rent-seeking. Blockchain has the ability to condense these multi-party markets into just two parties: buyer and seller. All rent-seeking space will disappear.

Blockchain can do more than just disrupt existing markets. If historically illiquid assets (such as loans) and their performance history are put on-chain, blockchain can bring unprecedented liquidity to these markets. This liquidity, combined with the ability to achieve true digital completeness and controllability of assets, will open up financing opportunities that were previously inaccessible. The disruptive opportunities brought by blockchain are significant, but the opportunities it creates for new development are even greater.

This was my "aha" moment. You can create native digital assets, and everyone can know the true ownership, composition, and history without relying on trust. Assets can be traded in real time, bilaterally, with no counterparty or settlement risk. Lenders can instantly and truly achieve complete digital control over collateral. Blockchain completely reshapes how assets are originated, traded, and financed. This is not a "lipstick on a pig" fintech makeover of old things, but an entirely new capital markets ecosystem. I want to be at the forefront of driving this transformation.

Figure: Reshaping Capital Markets with Blockchain

In early 2018, I co-founded Figure with my wife June Ou and several like-minded partners. Figure's goal is simple: to change capital markets with blockchain. To achieve this, we had to bring a real and measurable use case to the market.

Crypto companies once raised funds by selling tokens, but we chose a different path. We believed we could originate, aggregate, and securitize loans on blockchain, saving up to 85 basis points (bps) in transaction costs. We took this idea to banks, and they all said: "Great! We love it! We want to be the 10th bank to do this..." Clearly, this was not a "build it and they will come" situation—just building the system wouldn't bring people in on its own.

After leading a top lending business at SoFi, we weren't excited about creating another lending institution, but we also realized we had to prove to the market that blockchain would be better. In 2018, we became one of the first teams to originate consumer loans on-chain. Figure started as a direct-to-consumer loan originator, but with blockchain as the foundation. We chose home equity line of credit (HELOC) as our first product because we felt no one was originating it efficiently (greenfield), and we didn't want to immediately go head-to-head with major consumer loan or mortgage originators—we needed time to convince both sides of the market to adopt this new technology.

Soon we expanded the model to B2B2C. Today, more than 168 third parties use our technology to originate loans on-chain, including half of the top 20 retail mortgage institutions. Recently, we opened up blockchain-native capital markets to these originators: with our technology, they can sell assets directly, bilaterally, to the blockchain capital market (and soon, finance as well), without Figure acting as an intermediary.

In 2020, we completed the industry's first blockchain-native consumer loan securitization; in 2023, we completed the industry's first AAA-rated securitization. Since launch, we have originated over $15 billions in loans on-chain and completed more than $50 billions in on-chain transactions. We are the largest participant in the RWA field on public blockchains, and no one has caught up to us yet.

In 2018, most mainstream blockchains were based on PoW (Proof of Work). PoW does present challenges for financial services: cost, speed, and most importantly, predictability. PoS (Proof of Stake) was just beginning to rise at the time and could better address these issues. After a misjudged experiment with a quasi-permissioned chain, June and her team built and launched Provenance Blockchain. Provenance is a public, PoS, decentralized blockchain. Figure does not control Provenance, although we hold 20% of the utility token $HASH and continue to support the protocol's development. Provenance was built for financial services and is crucial for driving institutional adoption.

Blockchain and Capital Markets

We believe blockchain brings three core values to capital markets. The first is at the transaction level—reducing costs for auditing, quality control, third-party reviews, etc.; we have already benefited significantly here. The second is liquidity—supporting 24/7, real-time bilateral markets. Together with our partners, we are building such a greenfield loan trading market. Finally, there is financing, which we believe is the greatest value.

Putting native digital assets (such as loans) on-chain allows lenders to perfect their security interests (for example, through Figure's Digital Asset Registration Technology, DART) and gain control. Lenders can directly assess the liquidity, volatility, and advance rates of collateral to judge risk, rather than just underwriting the borrower. When we directly connect the supply and demand sides of capital, we can build a Pareto-efficient market: both lenders and borrowers benefit because they no longer bear the inefficient costs of capital allocators and other intermediaries. We first applied this decentralized (DeFi) approach to our crypto exchange to provide margin financing, and recently brought Figure's loans into our DeFi lending market—Democratized Prime. Just as we have demonstrated DeFi's power in trading/liquidity, we are now showcasing its power in financing with our own assets.

We have always believed that DeFi will eventually become the mainstream way to finance assets, and recent legislation is accelerating this process. After the GENIUS Act was passed, the US Treasury pointed out that trillions of dollars could flow into US Treasury notes via stablecoins. These funds will mainly come from bank deposits. In 2022–2023, $1 trillion in bank deposit outflows nearly broke the financial system. If the Treasury's judgment on scale and path is correct, something new must fill the gap. We believe that is DeFi, and we are leading the way in the RWA field.

The "Endgame" of Blockchain

We believe blockchain's value proposition can extend to all asset classes. Take public stocks, for example: beyond trading efficiency and liquidity, blockchain's improvements in financing may be the most significant right now. Imagine a scenario where you can seamlessly cross-collateralize stocks with other non-equity assets to gain leverage; or where investors themselves directly control and earn the economic benefits from lending out their stocks. Blockchain is the great equalizer in the financial arena. We pioneered lending on-chain, and next we hope to lead in bringing new asset classes (such as stocks) on-chain as well.

Just as Web 2.0 has the seven giant stocks today, I believe Web 3.0 will also have a group of peer companies representing blockchain technology. Our IPO brings us closer to becoming a leader among this peer group. Even though we have built a profitable and rapidly growing blockchain-based company in an extremely strict regulatory environment, we remain very optimistic: regulatory changes and public market acceptance of blockchain will, in the coming years, drive the entire industry and its opportunities. The IPO is just one step in the long process of bringing blockchain into every aspect of capital markets.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Kodiak launches Berachain native perpetual contract platform—Kodiak Perps, enhancing its liquidity ecosystem

The native liquidity platform of the Berachain ecosystem, Kodiak, recently launched a new product, Kodiak Perps,...

Mars Morning News | Michael Saylor calls: Buy Bitcoin now

Trump Media & Technology Group’s Q3 losses widened to $54.8 million, and it holds substantial amounts of bitcoin and CRO tokens; US consumer confidence has fallen to a historic low; a whale bought the dip in ZEC and made a profit; a bitcoin whale transferred assets; Michael Saylor called for buying bitcoin; the Federal Reserve may initiate bond purchases. Summary generated by Mars AI. The accuracy and completeness of this content is still being iteratively updated by the Mars AI model.

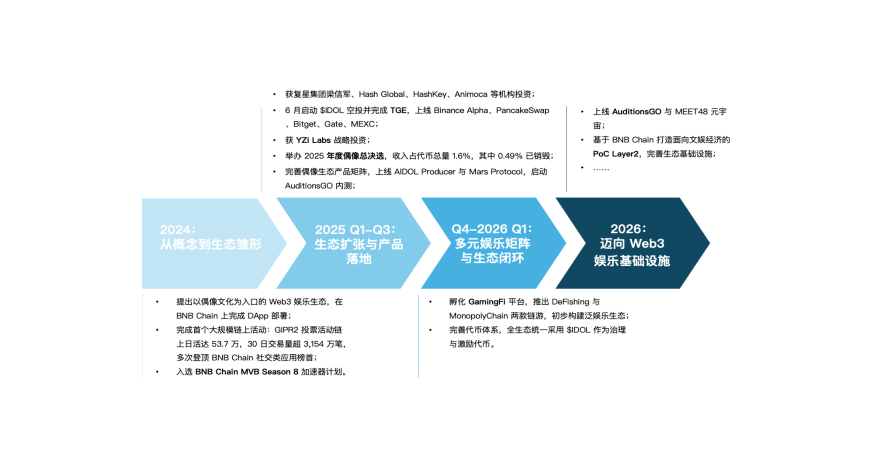

MEET48: From Star-Making Factory to On-Chain Netflix — How AIUGC and Web3 Are Reshaping the Entertainment Economy

Web3 entertainment is moving from the retreat of the bubble to a moment of restart. Projects represented by MEET48 are reshaping content production and value distribution paradigms through the integration of AI, Web3, and UGC technologies. They are building sustainable token economies, evolving from applications to infrastructure, aiming to become the "Netflix on-chain" and driving large-scale adoption of Web3 entertainment.

Digital Euro: Italy Advocates for a Gradual Implementation