Can stablecoins become the true pillar of US dollar hegemony?

Author: Spyros Andreopoulos

Translation: TechFlow

Original Title: Stablecoins Cannot Save Dollar Hegemony

In the short term, the growth of stablecoins may ease the fiscal constraints of the United States and further consolidate the dollar's position as the dominant currency. However, in the long run, stablecoins merely add another layer of complexity to the discussion about the quality of U.S. institutions.

Ultimately, what determines the dollar's status is still the fiscal soundness of the United States and the ability of its central bank to maintain low and stable inflation.

Source: Photo by SpaceX on Unsplash

The Trump administration seems to have high hopes for expanding stablecoin demand to make up for the federal fiscal deficit—a demand that is one of the main official reasons for the U.S. Treasury to shorten the average maturity of its debt (by issuing more Treasury bills while keeping the volume of notes and bonds unchanged).

By the way, I believe that shortening the average maturity of debt is also a way to increase pressure on the Federal Reserve to lower interest rates.

There is also some evidence that the demand for stablecoins has already lowered the interest rates on U.S. short-term debt.

In addition, the government views stablecoin demand as a major pillar supporting the dollar's dominant currency status.

The reason is not hard to understand.

Treasury Secretary Bessent predicts that the scale of stablecoins will grow to $2 trillion (I have even seen higher numbers). Since the vast majority of stablecoins are pegged to the dollar, the demand for stablecoins is very likely to be demand for dollars.

According to the GENIUS Act, U.S. dollar cash, insured domestic bank deposits, and Treasury securities with a remaining maturity of no more than 93 days are listed as permissible reserve instruments, so a large part of this demand will flow into federal debt.

From a purely domestic U.S. perspective, whether stablecoins will actually increase net demand for Treasuries is still inconclusive—it depends on what stablecoins are actually replacing.

If people do not hold shares in money market funds invested in short-term U.S. government bonds, but instead hold part of their wealth in stablecoins, then net demand for Treasury bills will not actually increase.

My intuition—so far, no more than that—is that the most important channel for generating net demand for dollars and U.S. Treasuries is the international channel: the dollarization channel of stablecoin demand.

Stablecoins make it easier for millions of people outside the United States to access dollars, especially in countries with high inflation, weak currencies, and underdeveloped banking systems.

That said, the growth in demand for stablecoins from the non-U.S. private sector may be partially offset by a decline in official demand for dollars. Why?

Stablecoins seem likely to improve global financial stability by increasing the share of dollar assets on balance sheets outside the United States. However, if this is the case, it may reduce currency mismatches in emerging market countries, and currency mismatch is one of the main reasons for the precautionary demand for dollars by official sectors in emerging markets.

On the Institutional Foundation of the Dollar Again

However, I have deeper concerns about the extent to which stablecoin demand helps the dollar's role. This relates to the dollar itself and the institutions that underpin it.

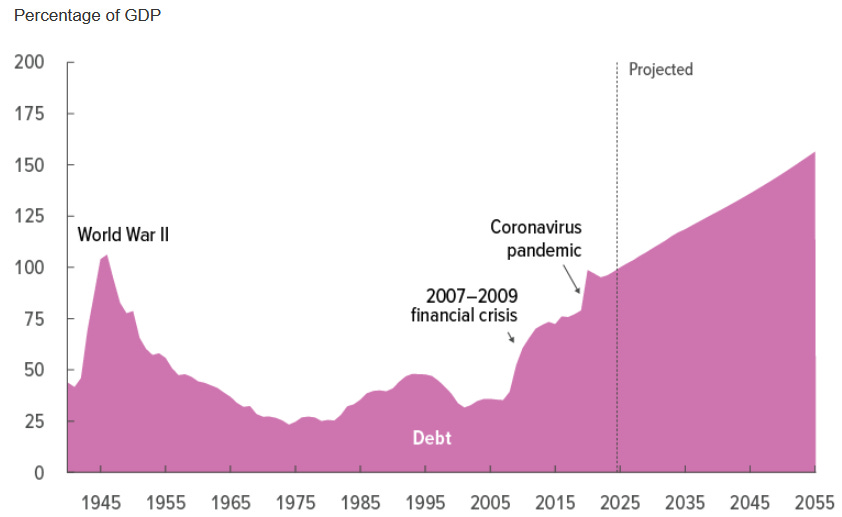

The U.S. fiscal situation is well known and will not be elaborated here.

Source: Congressional Budget Office (March 2025)

As a European who has long admired the United States, I may not be alone in diagnosing a "fiscal doomsday machine" triggered by political division.

One key reason this "doomsday machine" can keep running is the United States' dominant currency status and the resulting demand for U.S. government assets: the dollar's "exorbitant privilege" expands the U.S. federal government's fiscal space.

But ultimately, this does not alleviate the need for fundamental fiscal reform. This reform should mainly focus on increasing federal revenue (by the way, this is the opposite of the situation in Europe, where fiscal reform should focus on cutting spending).

Now, back to stablecoins.

The increased demand for U.S. government debt from stablecoins may relax fiscal policy constraints in the short term. But this does not solve any long-term problems—it cannot destroy this doomsday machine.

In fact, it is more likely to hinder the much-needed fiscal reform.

In other words, I worry that stablecoins may just be the rope American politicians use to hang themselves—and the resulting exorbitant privilege.

Then there is the Federal Reserve.

I have always believed that, given the relatively loose constraints that exorbitant privilege places on fiscal authorities, monetary policy must also be constrained: monetary policy cannot yield to the demands of fiscal policy (as Trump and his campaign have claimed). A necessary (though not sufficient) institutional condition to avoid this is the independence of the Federal Reserve.

The point here is that if the Fed's independence is weakened during this period and leads to higher inflation, then stablecoins will ultimately be of no help to the dollar's status.

The Endorsement of Stablecoins

Ultimately, as Pierpaolo Benigno said, the key lies in how stablecoins are endorsed.

In a monetary-dominant regime (i.e., the central bank provides price stability, while the fiscal authority is solely responsible for debt sustainability), stablecoins and the Treasuries behind them are ultimately supported by taxes: "To make stablecoins safe, the Treasuries themselves must be safe."

In a fiscally dominant regime, stablecoins are ultimately supported by the central bank. In this case, stablecoins may trigger inflation because the Fed may be forced to monetize the corresponding issuance.

My conclusion is that, although in the short term, the growth of stablecoins may ease the fiscal constraints of the United States and enhance the dollar's dominant currency status, in the long run, stablecoins merely add another layer of complexity to the discussion about the quality of U.S. institutions. Ultimately, what determines whether the dollar can maintain its status is still the fiscal soundness of the United States and the ability of its central bank to provide low and stable inflation.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Decoding VitaDAO: A Paradigm Revolution in Decentralized Science

Mars Morning News | ETH returns to $3,000, extreme fear sentiment has passed

The Federal Reserve's Beige Book shows little change in U.S. economic activity, with increasing divergence in the consumer market. JPMorgan predicts a Fed rate cut in December. Nasdaq has applied to increase the position limit for BlackRock's Bitcoin ETF options. ETH has returned to $3,000, signaling a recovery in market sentiment. Hyperliquid has sparked controversy due to a token symbol change. Binance faces a $1 billion terrorism-related lawsuit. Securitize has received EU approval to operate a tokenization trading system. The Tether CEO responded to S&P's credit rating downgrade. Large Bitcoin holders are increasing deposits to exchanges. Summary generated by Mars AI. The accuracy and completeness of this summary are still being iteratively improved by the Mars AI model.

The central bank sets a major tone on stablecoins for the first time—where will the market go next?

The People's Bank of China held a meeting to crack down on virtual currency trading and speculation, clearly defining stablecoins as a form of virtual currency with risks of illegal financial activities, and emphasized the continued prohibition of all virtual currency-related businesses.