The Journey of Hyperliquid (Part 3): No Battles in CLOB

Why the CLOB (Central Limit Order Book) architecture is suitable for perpetual contracts, and where are the limits of the CLOB architecture?

Why is the CLOB architecture (Central Limit Order Book) suitable for perpetual contracts, and where are the limits of the CLOB architecture?

Written by: Zuoye

The Binance life is a cover for Aster’s counter-exploitation, with an extreme wealth effect. Even emotions, in the drizzly late autumn, are enough to make people forget the troubles of their positions, regardless of being long or short.

Beyond the technical parameters and fee table comparisons, what truly piques my curiosity is why the CLOB architecture (Central Limit Order Book) is suitable for perpetual contracts, and where its limits lie.

Assets Determine Price

I was born too late to catch the era of DeFi Summer; I was born too early to see CLOB shine among foreign exchanges.

The history of traditional finance is so long that people have forgotten how markets were actually formed.

In short, finance revolves around the trading of assets and prices: price (buy/sell, long/short), assets (spot/contract/options/prediction). Cryptocurrency has merely replayed several centuries of financial history in just over a decade, adding its own unique needs or so-called improvements along the way.

CLOB is not simply an imitation of Nasdaq or CME. Breaking down the term, central, limit, and order book each occur on-chain, ultimately contributing to today’s prosperity.

1. Order Book: The mechanism for recording buy/sell prices.

2. On-chain Limit Order Book: A bidding mechanism sorted by both time and price, with “limit” referring to price limits.

3. On-chain Central Limit Order Book: Refers to recording limit orders in a unified system, such as a blockchain, which is what “central” means here.

CME, Binance, and Hyperliquid’s BTC contracts can all be CLOBs, but in this article, it specifically refers to CLOB Perp DEXs built on public chains/L2 architectures.

Following the third point, here’s a historical explanation: the debate over technical routes is a continuation of the high cost and slow speed issues of the ETH mainnet around 2021. Because of the FTX collapse in 2022, the Perp War that began at the end of DeFi Summer was postponed to 2025.

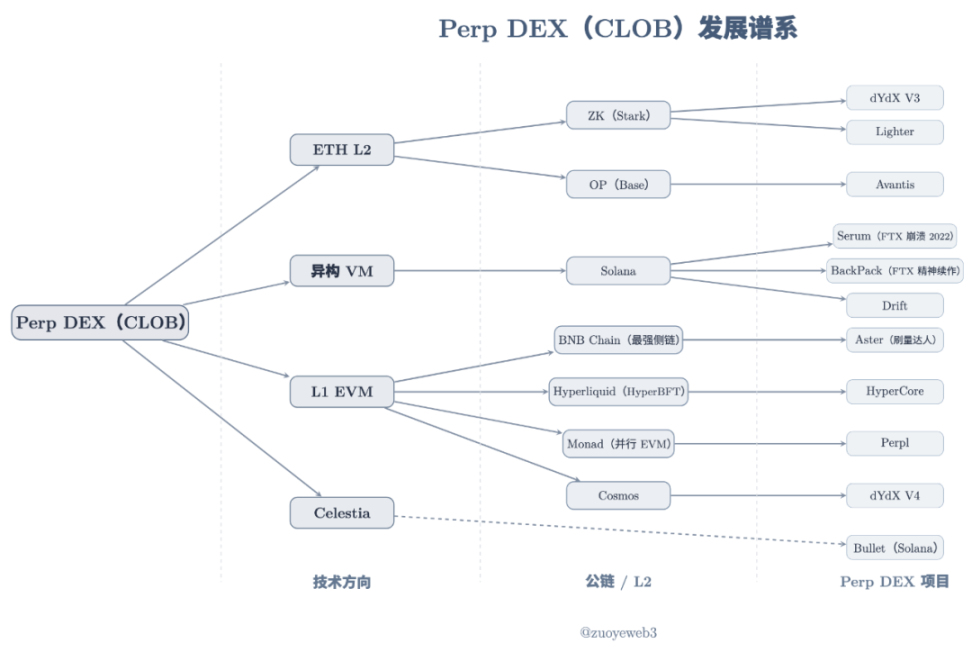

Image description: Perp DEX (CLOB) genealogy

Image source: @zuoyeweb3

Perp DEX projects launched at different times, but can basically be divided into three routes: ETH L2, heterogeneous VM (Solana), and L1 EVM. Celestia is a DA solution that doesn’t rely on a specific VM architecture.

Historical documents are not practically significant; currently, people don’t care about decentralization, only about trading efficiency, so there’s no need to compare. Whether it’s Hyperliquid’s 4–>16–>24 nodes or the generally single sequencer L2s, it’s hard to say which is faster or more decentralized, or what the point is.

Human sorrow is not shared; I just find their quarrels noisy.

There is a lag in technological investment. The seeds for DeFi Summer in 2020 were sown in 2017/18. By the end of 2020, Serum had already started slowly on Solana, with the following features:

1. Liquidity frontend and profit sharing

2. Expected support for spot trading

3. Relies on Solana’s high-performance matching engine

4. Node locking to earn MegaSerum (MSRM)

5. Collaboration with FTX

6. Cooperation with Wormhole to support cross-chain

7. Yield mechanism for cross-chain assets

8. SRM fee discounts

9. SRM buyback and burn mechanism

10. Expected SerumUSD stablecoin product line

Of course, the vast majority of SRM tokens were not distributed but concentrated in the hands of FTX and even SBF personally. The collapse in 2022 gave Hyperliquid more time to develop itself.

This is not to say that Hyperliquid is a copy of Serum. Any great product is either an engineering combination or original spirit. Hyperliquid is far superior to Serum in technical selection, joint market making for liquidity, token airdrops, and risk control.

From dYdX/Serum to Hyperliquid, everyone agrees that moving Perp asset types on-chain is feasible. The differences lie in technical architecture, decentralization, and liquidity organization, but it still doesn’t answer what features of CLOB led to this consensus.

So, why does the Perp asset choose CLOB?

The most reasonable answer is that CLOB has stronger price discovery capabilities.

This is still a historical answer and is related to AMM DEXs. From Bancor to Uniswap and Curve, explorations around Ethereum have opened up on-chain liquidity initialization and applicability.

DEX protocols, through LPs (liquidity providers), avoid the two major problems of custodial user funds and maintaining liquidity, focusing only on protocol security. LPs, incentivized by fee sharing, deploy liquidity themselves.

Subsequently, LPs ultimately transfer liquidity costs to users, reflected in slippage and fees. That is, liquidity creation: DEX protocol to LP, LP to user.

However, two problems remain: LP’s impermanent loss and AMM’s insufficient price discovery.

- The root of impermanent loss lies in the exchange of two assets. LPs need to add dual assets equally, but the trends of the two are inconsistent. Most are stablecoin pairs to enhance stability.

- AMM’s price is a “market price,” meaning neither LPs, project parties, nor DEX protocols can directly define the price of an asset, only intervene through liquidity.

To address these two issues, the former is improved by Curve’s USDC/USDT stablecoin trading, minimizing dual asset changes and relying on increased trading frequency to boost fees. Rather than saying Curve is suitable for stablecoin pairs as a feature, it’s more of an inherent flaw. Its latest work, Yield Basis, uses economic design and leverage to “erase” impermanent loss.

The latter’s improvement limit is CoW Swap’s TWAP (Time-Weighted Average Price), which splits large orders into multiple small ones to reduce the impact on liquidity and obtain the best execution price—Vitalik’s favorite.

But that’s the limit. For on-chain Perp trading, transaction details are open and transparent. If using the AMM mechanism, it’s very easy to manipulate prices by adjusting liquidity. A 1% price move is explainable for spot trading, but for Perp, it’s a ticket to heaven.

The shortcomings of AMM mean it cannot, or at least cannot on a large scale, be used for Perp. A technology that controls price without relying on liquidity changes is needed—that is, prices must be preset.

Trades must be executed at the quoted price or not at all, but cannot be executed at a discount, to maintain the normal operation of the Perp market.

Eliminating impermanent loss is just a side effect. Different technical architectures lead to different market-making mechanisms.

The price sensitivity of Perp and the precise control of CLOB are a perfect match—assets determine price changes, and price changes require corresponding technical architecture.

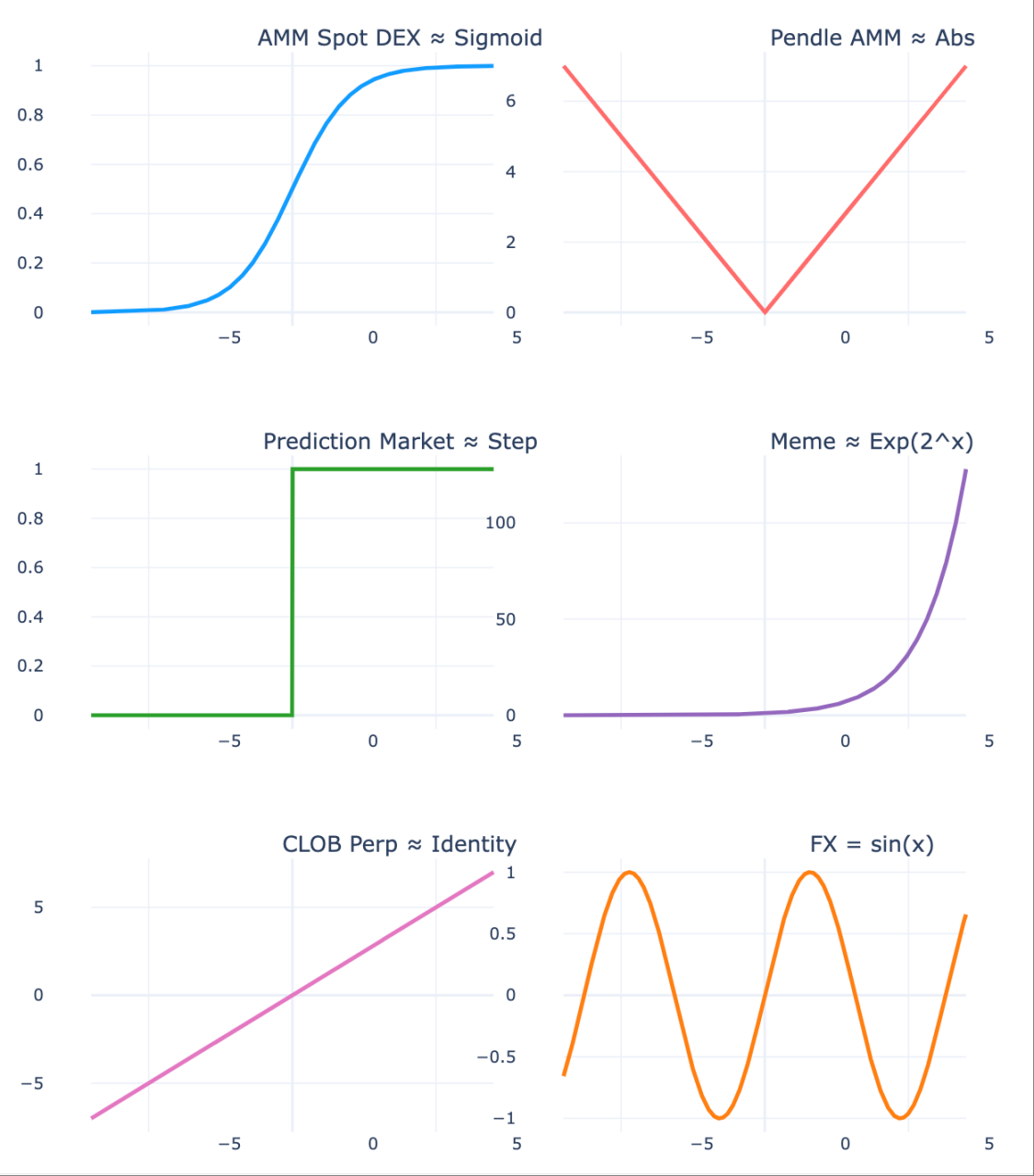

Image description: Assets determine price trends

Image source: @zuoyeweb3

- Spot price trends are relatively smooth, which is why users can “tolerate” slippage and LPs can “tolerate” impermanent loss—there’s not much loss.

- Pendle creates two different price trends by splitting assets by maturity, leading to different side bets on liquidity in the market.

- Prediction markets are more extreme, with only (0,1) outcomes—the most discrete existence, where continuous probabilities ultimately collapse to 0/1.

- Meme markets are even more extreme—a few assets experience extreme index changes, while most become illiquid assets trending toward zero, matching the theory of internal and external markets.

- Perpetual contracts are the most extreme, and can even result in negative balances, as their price changes are not only drastic but also do not stop at zero, continuing downward.

- Forex trading has the smallest price changes, with daily price fluctuations within a range, sometimes even showing patterns, reflecting the stability of major global economies.

AMM created initial on-chain liquidity, cultivated trading habits and capital accumulation, while CLOB is more suitable for price control and complex trading setups. Unlike AMM’s market price, CLOB uses time–price sorted bids and asks, and with efficient algorithms, achieves precise price discovery.

Price Determines Liquidity

A lifetime is said, but if it’s short by a year, a month, a day, or even an hour, it’s not a lifetime.

After CLOB replaces AMM and completes price discovery for Perp, it still needs to organize market liquidity. AMM DEXs achieve the normalization of individual LPs through two rounds of transfer (protocol to LP, LP to user).

But between price and liquidity, there is also the scale phenomenon unique to Perp.

The issues of Perp DEX are relatively complex. For AMM, gains and losses are only calculated upon final execution; otherwise, both users and LPs are only marking floating profits and losses. The focus of perpetual contracts is not the contract, but the perpetual nature.

There is a funding rate mechanism between longs and shorts: when the rate is positive, longs pay shorts; when negative, shorts pay longs.

From a pricing mechanism perspective, this keeps contract prices in line with spot prices. When the contract price is below spot, it indicates a bearish market, so longs must pay shorts to maintain the market’s existence—otherwise, with no shorts, there would be no perpetual contract market, and vice versa.

As mentioned earlier, AMM is a trade between two assets, but for USDC-margined BTC contracts, there is no need to exchange BTC itself, but rather expectations of BTC’s price, conventionally denominated in USDC to reduce volatility.

This expectation requires two things:

1. The spot asset must achieve price discovery, such as a fully traded BTC market. The more mainstream the coin, the more fully its price is discovered, making black swan events less likely;

2. Both long and short sides must have strong capital reserves to offset extreme events caused by leverage, and be able to handle such events effectively.

That is, the price mechanism of Perp tends to increase market scale, and this scale drives liquidity.

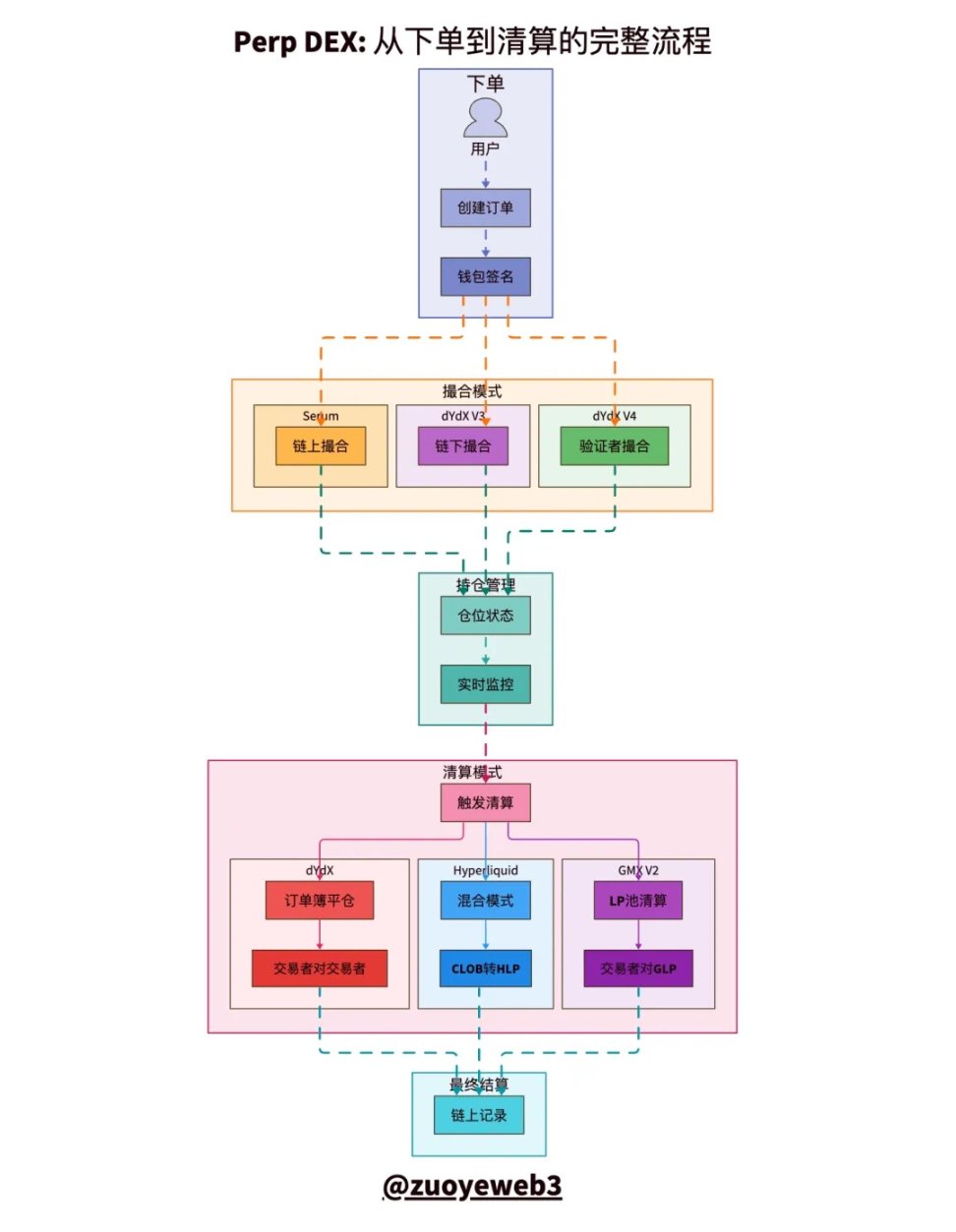

Image description: CLOB clearing and settlement process comparison

Image source: @zuoyeweb3

The entire Perp trading process can be divided into five parts: order placement, matching, holding positions, liquidation, and settlement. The most difficult are the matching and liquidation mechanisms.

- Matching is a technical issue—how to match buy/sell orders with maximum efficiency and minimum time. The market ultimately chooses “centralization.”

- Liquidation is an economic issue. Contracts can be understood as under-collateralized loans; exchanges allow you to use a small amount of principal to leverage large positions, which is the essence of leverage.

On the surface, exchanges allow you to use collateral to increase leverage, but in reality, you must pay margin to maintain leverage. Once you fall below the liquidation ratio, the exchange takes your collateral.

Internally, liquidation is a natural behavior between longs and shorts under normal circumstances. But as mentioned earlier, Perp prices can go below zero indefinitely, and with leverage amplification, debts can far exceed the value of collateral.

If the market cannot clear bad debts, manual margin replenishment, forced trade cancellation, or insurance funds are needed to cover losses. But essentially, this is socializing the debt—everyone bears it together.

Perp’s liquidity is a necessary pursuit to maintain scale, but the task cannot be accomplished by individual AMM LPs. Besides capital limitations, it requires the high-frequency trading expertise of professional market makers.

The logic is simple: individual LPs providing liquidity on AMM DEXs don’t need to operate frequently, but Perp DEXs must always be alert to leverage extremes.

During normal trading, as long as extreme events are not triggered, there are mechanisms similar to AMM’s LP incentives to boost trading volume. For example, GMX imitates AMM DEX’s LP mechanism, using its own token to incentivize LP trading activity, developing its own GLP pool, where users can add liquidity and earn fees and other rewards.

This is actually a very “innovative” mechanism, allowing individual LPs to participate in Perp market making for the first time.

This wash trading mechanism leads to abnormally high Perp trading volume (Volume), but OI (Open Interest) drops after token issuance as LPs withdraw, eventually entering a death spiral of declining tokens and liquidity.

Another conclusion is that LPs must passively bear the final liquidation. This is a key difference between Perp and AMM: AMM users buy and walk away, LPs bear their own profits and losses, but Perp LPs must take on the project’s liquidation function, which cannot be transferred to users.

The so-called insurance mechanism only insures the project party, not the LPs themselves.

GMX and Aster’s wash trading will end quickly. Hyperliquid’s HLP runs stably in daily operations, but when facing $JELLYJELLY, HLP still bears the loss, which essentially shows the unreliability of such liquidity creation and insurance mechanisms.

As mentioned above, over 92% of HyperCore’s fees are used for $HYPE buybacks, and 8% for HLP profit sharing, indicating that Hyperliquid does not value the future of HLP and similar mechanisms. HyperCore’s liquidity is mainly maintained by professional market makers, who care about node profit sharing and $HYPE appreciation.

The insurance vault mechanism can be said to be an appendix Perp learned from AMM. Directly pulling the plug or increasing trading depth is more effective.

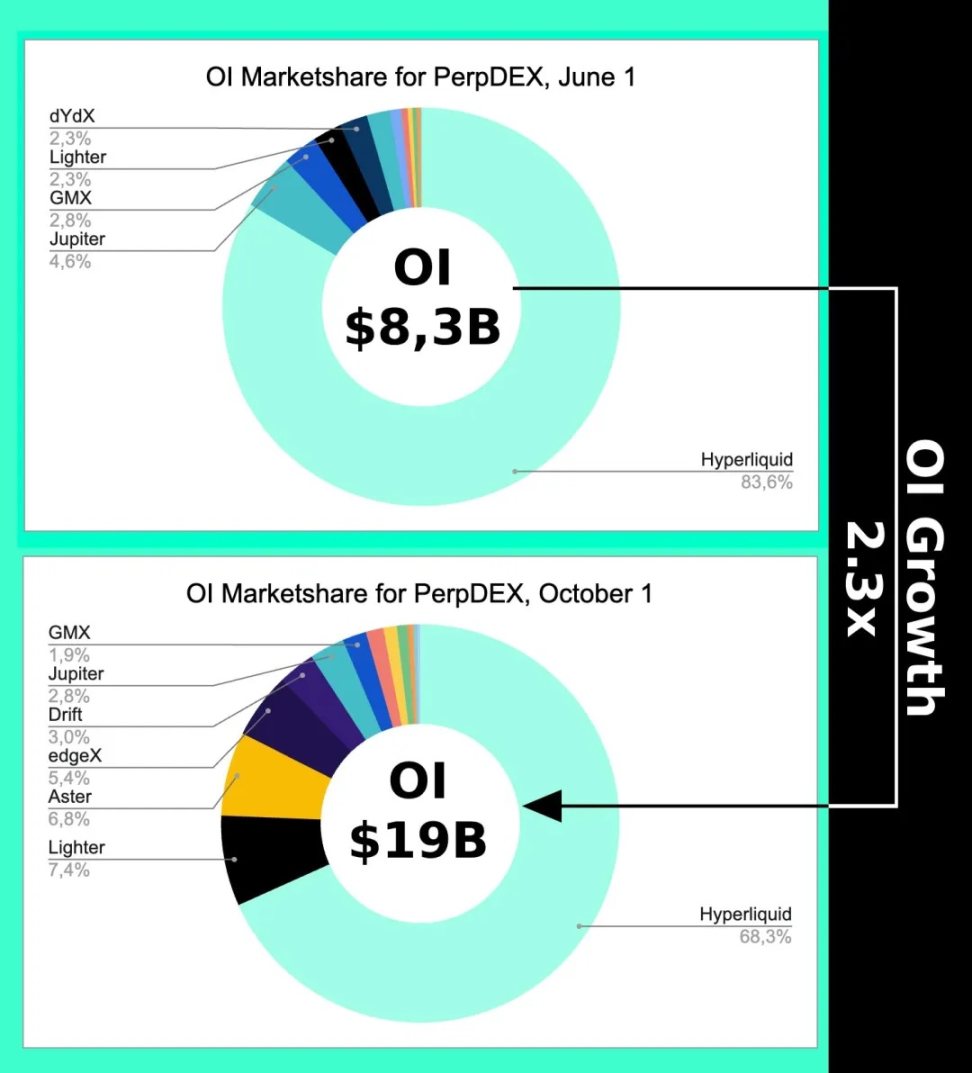

Image description: OI trend

Image source: @Eugene_Bulltime

Even at the peak of the Perp DEX war started by Aster in early October, Hyperliquid’s market share only dropped by about 15%, while Volume was overtaken by Aster several times over. This also shows that the CLOB price mechanism triggers a scale effect, and the resulting liquidity mainly refers to open interest, not trading volume.

This also indirectly explains why Hyperliquid is developing the Unit cross-chain bridge and BTC spot trading market—not for fees, but for price accuracy, to ultimately break away from reliance on Binance quotes.

CLOB can also be used for spot trading, and AMM modified by AC can also be used for perpetual contracts.

Focus on the fit between price and assets, don’t get lost in technical parameters.

Conclusion

Life will find its way out.

Binance’s annual 15 trillion USD is basically the upper limit for Perp trading, but the daily trading volume of the forex market is about 10 trillion USD, and the annual trading volume is 300 times that of Perp. Hyperliquid’s architecture is also migrating to HyperEVM, especially with the expected development of new assets such as forex, options, and prediction markets through HIP-3/4.

It can be understood that Perp will eventually reach its ceiling. In the competition between assets and prices, more suitable technical architectures for the new generation of asset price discovery mechanisms will emerge, such as RFQ.

But there is no doubt that it will no longer be a debate about blockchain centralization. The 2021 technical debate was just a boring call back. Focusing on blockchain technical architecture is essentially living in the past and unable to extricate oneself.

Regardless of whether OI or trading volume continues to grow, the CLOB debate is over. 2018 was DeFi Summer, and by 2022 Hyperliquid had already won. Next, we’ll see if HyperEVM can make it to the final public chain dinner. It remains to be seen whether Monad will still exist after its token launch, and whether HyperEVM can achieve an ecological closed loop—that’s what’s truly interesting.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

CARV In-Depth Analysis: Cashie 2.0 Integrates x402, Transforming Social Capital into On-Chain Value

It is no longer just a tool, but a protocol.

Trump Takes Control of the Federal Reserve: The Impact on Bitcoin in the Coming Months

The U.S. financial system is undergoing its most significant transformation in a century.

Castle Island Ventures partner: I don’t regret spending eight years in the cryptocurrency industry

Move forward with pragmatic optimism.

Undercurrents Surge: Crypto Whales Spark Another Wave of Accumulation