Will the Federal Reserve's monetary policy become ineffective in a market with distorted liquidity?

The decisive macroeconomic risk is no longer inflation, but "institutional fatigue."

The decisive macroeconomic risk is no longer inflation, but "institutional fatigue."

Written by: arndxt

Translated by: AididiaoJP, Foresight News

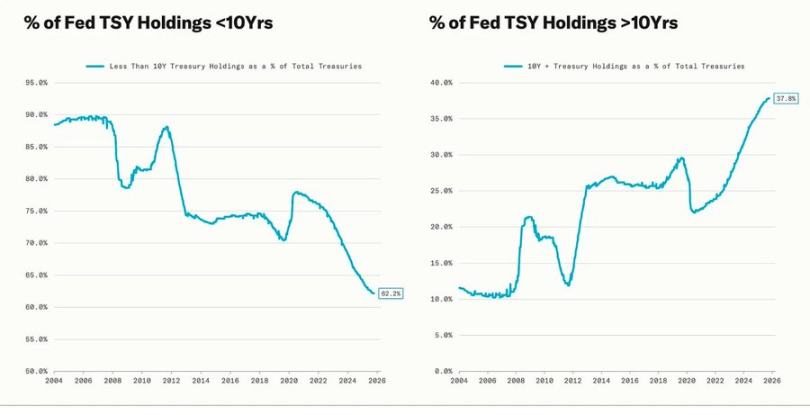

The several major downturns in the crypto market have coincided precisely with the Federal Reserve's "quantitative easing" phases. During these periods, the Fed deliberately suppressed long-term yields by extending the maturity of its asset holdings (these policies included "Operation Twist" and the second and third rounds of quantitative easing, i.e., QE2/QE3).

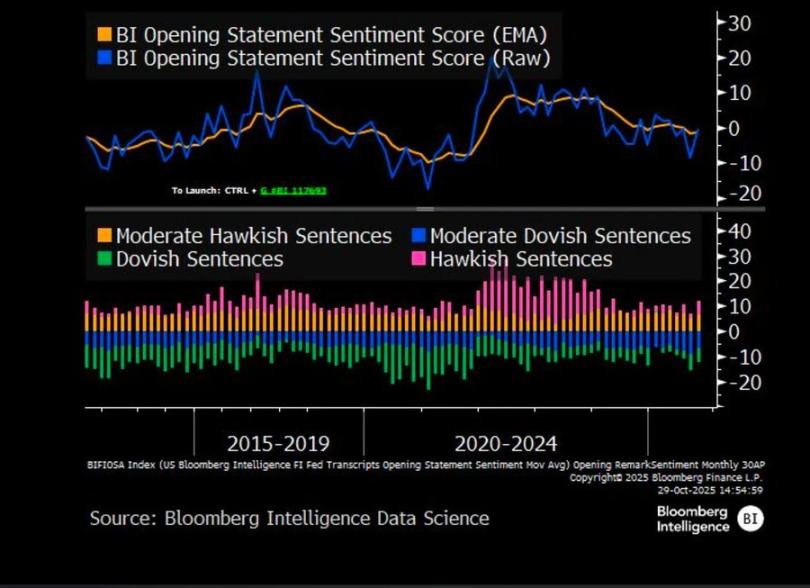

Powell stated that we are currently operating in a situation of incomplete information and unclear outlook, making slow and risky decisions. This goes beyond the Fed itself and accurately depicts the current global economic landscape. Policymakers, businesses, and investors are all moving forward with extremely low visibility, relying only on reflexive liquidity responses and short-term incentives to find their way.

We are now in a new policy environment characterized by uncertainty, fragile confidence, and markets distorted by liquidity.

The Fed's "Hawkish Rate Cut"

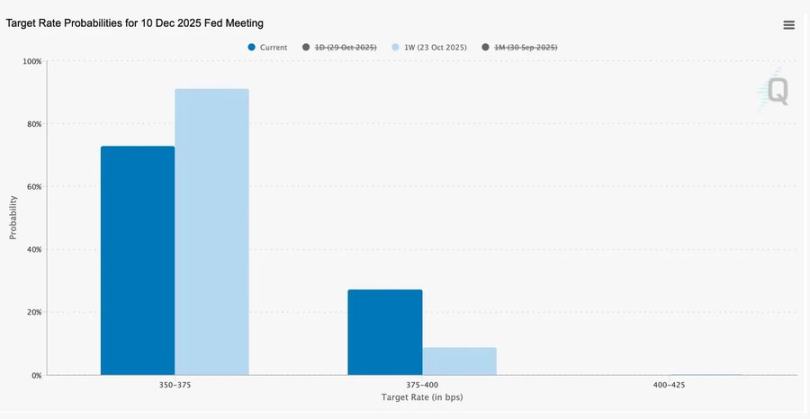

This "risk management" rate cut, lowering the interest rate range from 3.75%–4.00% by 25 basis points, is not simply about releasing liquidity, but rather about gaining more policy flexibility for the future.

Faced with two diametrically opposed dissenting opinions, Powell actually sent a clear message to the market: slow down, because visibility has disappeared.

The government shutdown, which interrupted economic data, has put the Fed in a highly uncertain predicament. Powell's hint to traders could not be clearer: do not assume a December rate cut is a given. After the market digested this shift from "data-dependent" to "data-deficient" caution, the probability expectation for a rate cut dropped sharply, causing the short-term yield curve to flatten.

2025: The "Hunger Games" of Liquidity

Repeated rescue actions by central banks around the world have institutionalized speculative behavior. Now, what determines asset performance is no longer productive efficiency, but liquidity. This mechanism continues to inflate asset valuations even as credit in the real economy remains weak.

The discussion further extends to a deeper examination of today's financial system architecture, mainly including three points: the concentration of passive investment, the reflexivity of algorithms, and retail investors' options frenzy:

Passive fund flows and quant funds dominate market liquidity; volatility is now determined by capital positioning, not economic fundamentals.

Retail investors' massive purchases of call options and the resulting "gamma squeeze" have created artificial upward price momentum in areas like "meme stocks"; meanwhile, institutional funds are crowding into a handful of leading stocks, making market leadership increasingly narrow.

Podcast hosts have dubbed this the "financial hunger games," where structural inequality and policy reflexivity are forcing smaller investors into speculative "survivalism."

Note: A gamma squeeze is a self-fulfilling cycle in financial markets where massive option buying "forces" stock prices higher.

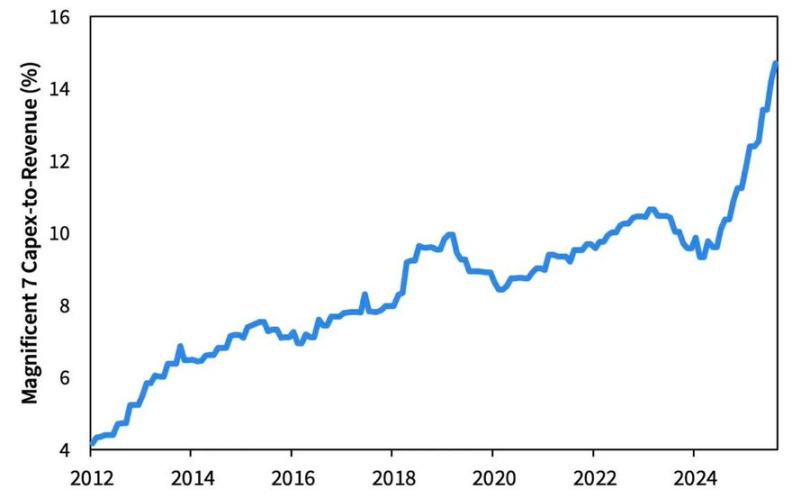

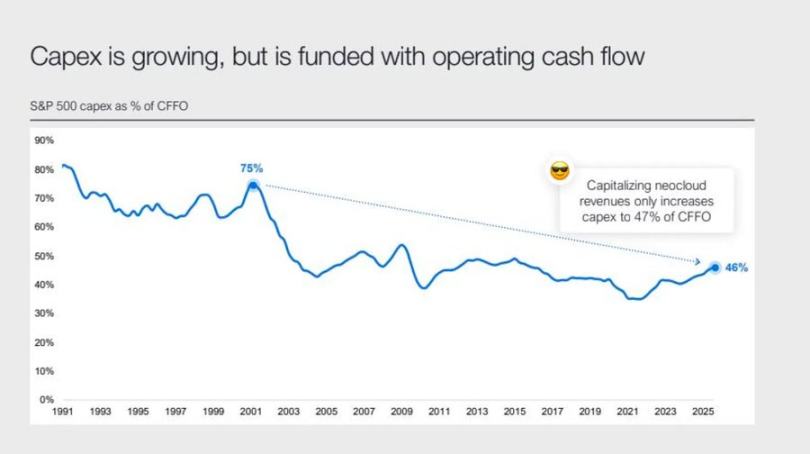

2026: Capital Expenditure Boom and Risks

The capital expenditure wave triggered by artificial intelligence seems to have pushed tech giants into the late-cycle stage of industrialization. For now, this is supported by liquidity, but in the future, it will be highly sensitive to leverage.

Although corporate profits remain impressive, a historic shift is underway beneath the surface: large tech companies are transforming from light-asset "money printers" into capital-intensive infrastructure operators.

This construction boom, driven by AI and data centers, was initially supported by companies' own cash flows, but now relies on record-breaking debt issuance for financing (for example, Meta's oversubscribed $25 billion bond issue).

This transformation means companies will face margin compression, rising depreciation expenses, and may ultimately come under refinancing pressure—potentially sowing the seeds for the next credit cycle turning point.

Trust, Inequality, and Policy Cycles

Policies that continuously bail out the largest market participants have intensified wealth concentration and damaged market integrity. The coordinated actions of the Fed and the Treasury, shifting from quantitative tightening to buying Treasury bills, have further reinforced this trend, ensuring ample liquidity at the top while ordinary households struggle under the dual pressures of stagnant wages and rising leverage.

Today, the decisive macroeconomic risk is no longer inflation, but "institutional fatigue." The market still appears prosperous on the surface, but faith in market fairness and transparency is deteriorating. This is the true systemic vulnerability of the 2020s.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Zuckerberg’s Threads starts 2026 ahead of Musk’s X in user count

Bitcoin Sees $1.65B Exodus From Exchanges as Holders Move to Cold Storage