After an 80% drop in stock price, is there a value mismatch in BitMine?

With the three main buying channels simultaneously under pressure and the staking ecosystem losing momentum, Ethereum's next stage of price support faces a structural test. Although BitMine is still buying, it is almost fighting alone. If even BitMine, the last pillar, can no longer buy, what the market stands to lose will not just be a single stock or a wave of capital, but potentially the very foundation of belief in the entire Ethereum narrative.

Author: Zhou, ChainCatcher

The crypto market remains sluggish. Since November, Ethereum's price has dropped by nearly 40% from its peak, and ETF outflows have continued. Amid this round of systemic downturn, the largest Ethereum treasury company, BitMine, has become a focal point. Founders Fund, under Peter Thiel, reduced its BMNR holdings by half, while at the same time, ARK Invest led by Cathie Wood and JPMorgan chose to increase their positions against the trend.

The diverging attitudes of capital have put BitMine's “5% Alchemy” on trial: 3.56 million ETH, a floating loss of 3.0 billions, mNAV dropping to 0.8. As one of the last bastions of Ethereum buying, how much longer can BitMine keep buying? Is there a value mismatch? After the DAT flywheel stalls, who will take over ETH?

I. BitMine's 5% Alchemy: How Long Can the Funds Last?

BitMine, as the second largest crypto treasury company after MicroStrategy, once planned to purchase tokens equivalent to 5% of Ethereum's total circulation in the future. On November 17, BitMine announced its Ethereum holdings had reached 3.56 million, accounting for nearly 3% of the circulating supply, more than halfway to its long-term goal of 6 million. In addition, the company currently holds about 11.8 billions USD in crypto assets and cash, including 192 bitcoins, 607 million USD in unencumbered cash, and 13.7 million shares of Eightco Holdings stock.

Since launching its large-scale coin accumulation plan in July, BitMine has become a market focus. During that period, the company's stock price rose in tandem with Ethereum, and the story of "raising market cap with coins" was seen by investors as a new model in the crypto space.

However, as the market cooled and liquidity tightened, sentiment began to reverse. Ethereum's price decline made BitMine's aggressive buying pace appear even riskier. Based on an average purchase price of 4,009 USD, BitMine's paper loss has approached 3.0 billions USD. Although Chairman Tom Lee has repeatedly expressed bullishness on Ethereum and stated that they will continue to buy at low prices, investors' focus has shifted from "how much more can they buy" to "how much longer can they last."

Currently, BitMine has about 607 million USD in cash reserves, with funds mainly coming from two channels.

First is crypto asset revenue. BitMine relies on immersion cooling bitcoin mining and consulting services for short-term cash flow, while staking Ethereum for long-term returns. The company claims its ETH holdings will be staked to generate about 400 million USD in net income.

Second is secondary market financing. The company launched an ATM stock sale plan, a mechanism that allows it to sell new shares for cash at any time without presetting price or scale. So far, the company has issued hundreds of millions of dollars in stock, attracting institutional funds including ARK, JPMorgan, Fidelity, and others. Tom Lee stated: When institutions buy large amounts of BMNR, those funds will be used to purchase ETH.

Through the dual engines of accumulating ETH and generating returns, BitMine attempts to reshape the logic of corporate capital allocation, but changes in the market environment are undermining the stability of this model.

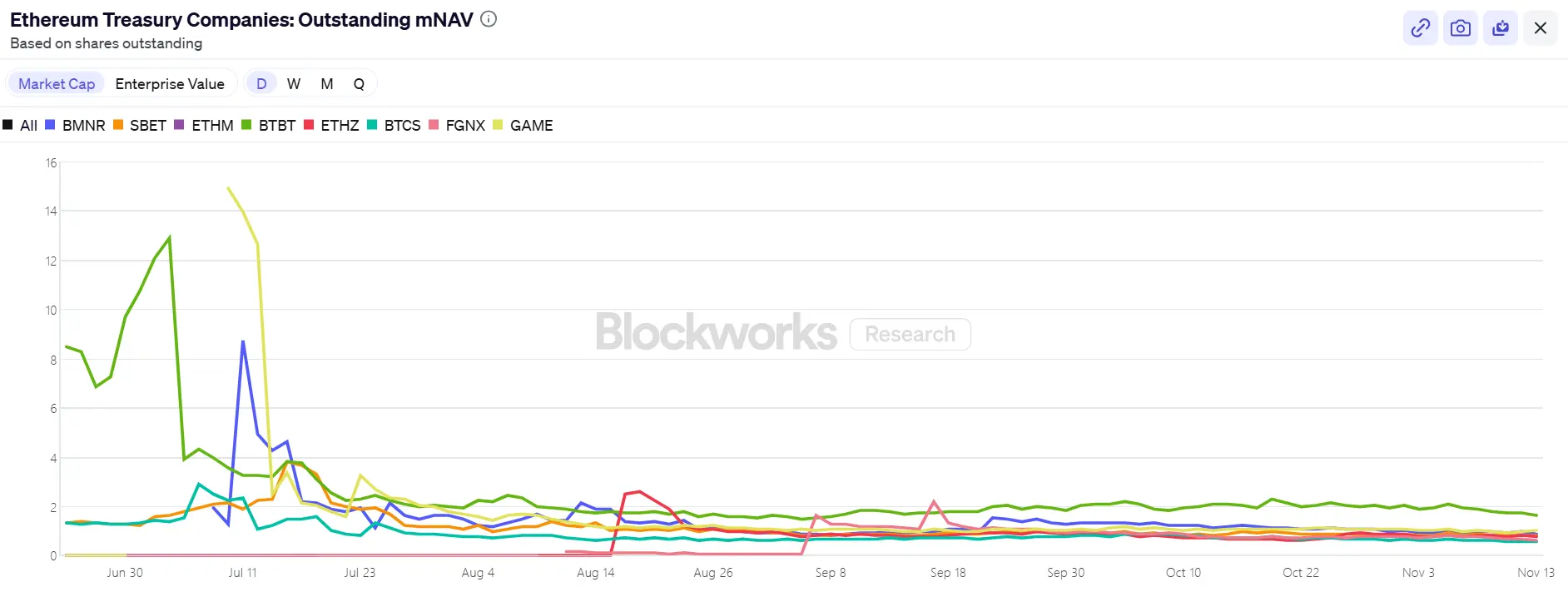

In terms of stock price, BitMine (BMNR) is under some pressure, having fallen about 80% from its July high, with a current market cap of about 9.2 billions USD, below its ETH holdings value of 10.6 billions USD (at ETH 3,000 USD), and mNAV dropping to 0.86. This discount reflects market concerns about the company's floating losses and funding sustainability.

II. The Last Straw for ETH Price: Three Major Buying Forces Diverge, Staking Retreats

From a macro perspective, the Federal Reserve has sent hawkish signals, the probability of a rate cut in December has fallen, the overall crypto market is weak, and risk appetite has dropped significantly.

Currently, ETH has dipped to 3,000 USD, down more than 30% from the August high of 4,900 USD. This round of correction has refocused the market on a key question: If the previous price support came from treasury companies and institutional accumulation, who will take over when buying dries up?

Among visible market forces, the three major buying sides—ETF, treasury companies, and on-chain funds—are diverging in different directions.

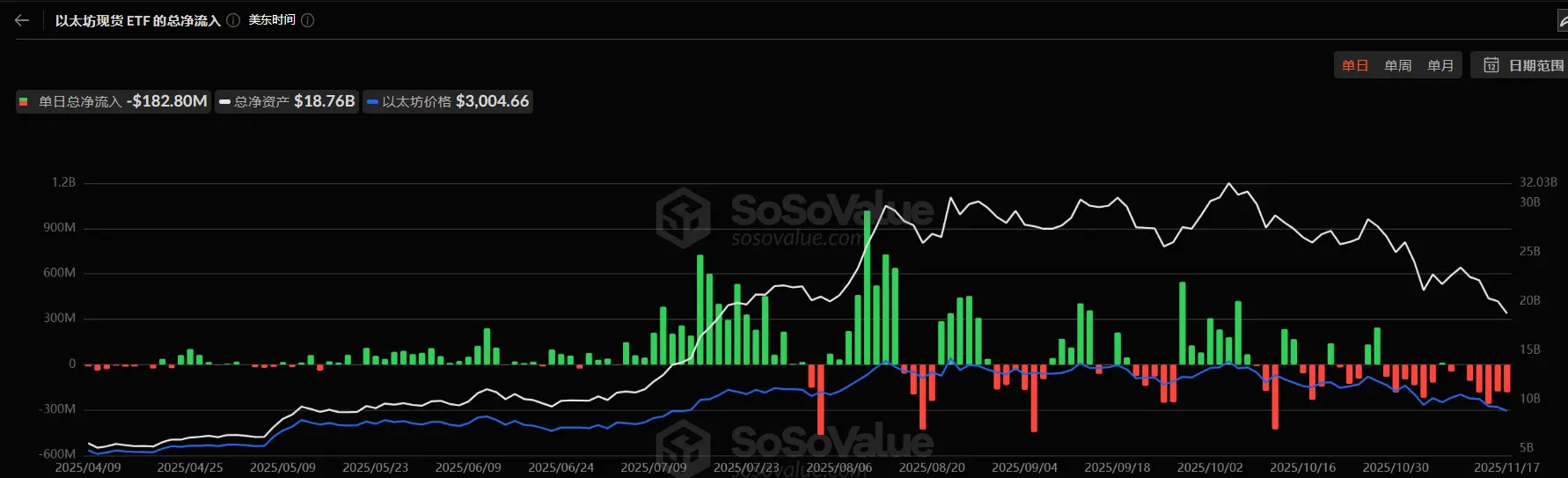

First, capital inflows into Ethereum-related ETFs have clearly slowed. Currently, ETF total holdings are about 6.3586 million ETH, accounting for 5.25% of total supply. According to SoSoValue data, as of mid-November, the total net assets of spot Ethereum ETFs were about 18.76 billions USD, with net outflows this month significantly exceeding inflows, and single-day outflows reaching as high as 180 million USD. Compared to the steady inflows from July to August, the capital curve has shifted from a steady rise to a volatile decline.

This decline not only weakens the potential power of major buyers but also reflects that market confidence has not fully recovered from the crash. ETF investors typically represent medium- to long-term allocation funds, and their withdrawal means incremental demand for Ethereum from traditional financial channels is slowing. When ETFs no longer provide upward momentum, they may instead amplify volatility in the short term.

Second, digital asset treasury (DAT) companies have also entered a stage of divergence. Currently, treasury companies' strategic Ethereum reserves total 6.2393 million ETH, accounting for 5.15% of supply. The pace of accumulation has clearly slowed in recent months, with BitMine almost the only major player still buying on a large scale. In the past week, BitMine increased its holdings by 67,021 ETH, continuing its buy-the-dip strategy; SharpLink has not made further purchases since buying 19,300 ETH on October 18, with an average cost of about 3,609 USD, and is also in a floating loss position.

In contrast, some small and medium treasury companies are being forced to contract. ETHZilla sold about 40,000 ETH at the end of October to buy back shares, attempting to narrow the discount range and stabilize the stock price by selling part of its ETH.

This divergence means the treasury industry is shifting from broad expansion to structural adjustment. Leading companies can still maintain buying thanks to capital and confidence, while small and medium companies are trapped by liquidity constraints and debt pressure. The market baton has shifted from widespread incremental buying to a few “lone warriors” with capital strength.

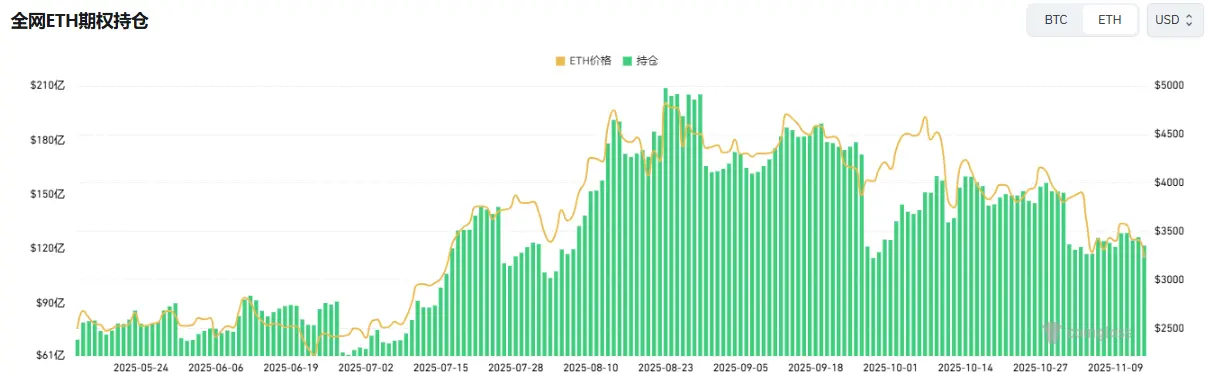

On the on-chain level, short-term capital is still dominated by whales and high-frequency addresses, but they do not provide price support. Recently, “Brother Machi,” who persisted in longing ETH, was liquidated several times, which to some extent hurt trading confidence. According to Coinglass data, ETH total contract open interest has nearly halved since the August high, and leveraged funds are shrinking rapidly, meaning both liquidity and speculative heat are cooling.

In addition, recently, Ethereum ICO wallet addresses dormant for over 10 years have been activated and started transferring out. Glassnode data reports that long-term holders (addresses holding for over 155 days) are currently selling about 45,000 ETH per day, equivalent to 140 million USD. This is the highest selling level since 2021, indicating that bullish forces are weakening.

BitMEX co-founder Arthur Hayes recently wrote that even though dollar liquidity has contracted since April 9, ETF inflows and DAT purchases allowed bitcoin to rise, but that state has ended. The basis is not rich enough for institutional investors to keep buying ETFs, and most DATs are trading at a discount to mNAV, so investors are now avoiding these derivative securities.

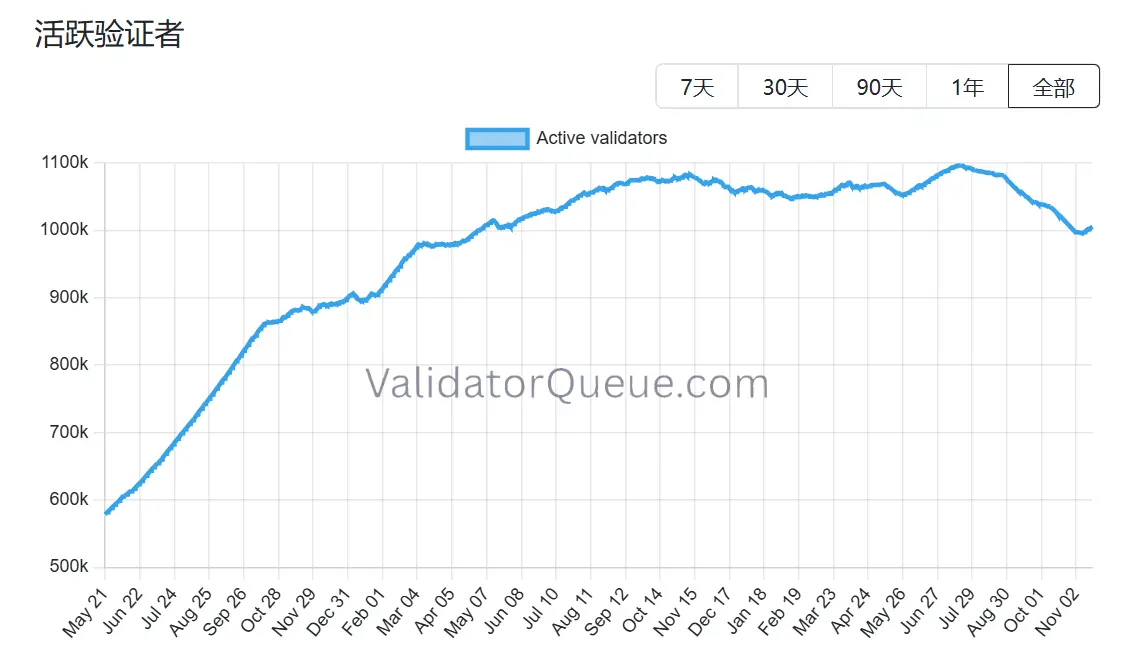

The same is true for Ethereum, especially as its staking ecosystem is also showing signs of retreat. Beaconchain data shows that the number of daily active Ethereum validators has dropped about 10% since July, falling to the lowest level since April 2024. This is the largest drop since the network switched from proof-of-work (PoW) to proof-of-stake (PoS) consensus in September 2022.

The decline is mainly due to two reasons:

The decline is mainly due to two reasons:

First, this year's Ethereum rally led to validator exit queues reaching unprecedented highs, as staking operators rushed to unstake and sell for profit.

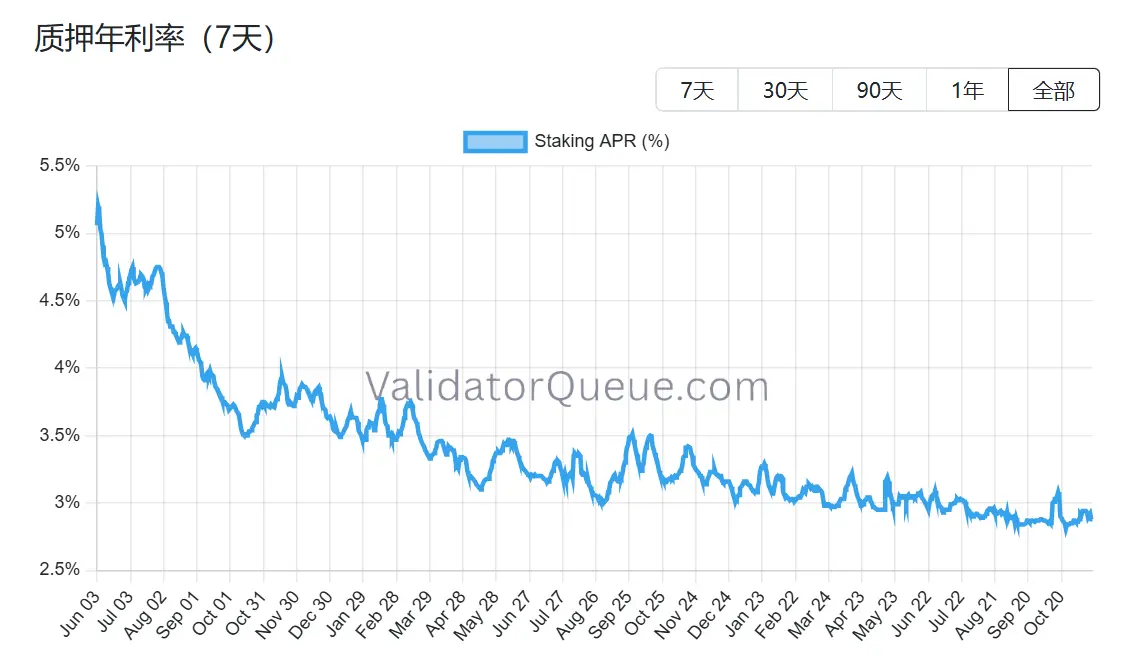

Second, staking yields have fallen and borrowing costs have risen, making leveraged staking unprofitable. Currently, Ethereum's annualized staking yield is about 2.9% APR, far below the historical high of 8.6% set in May 2023.

With all three major buying paths under simultaneous pressure and the staking ecosystem retreating, Ethereum's next stage of price support faces a structural test. BitMine is still buying, but is almost fighting alone. If even BitMine, the last pillar, can no longer buy, what the market loses will not just be a stock or a wave of capital, but possibly the very foundation of belief in the Ethereum narrative.

III. Does BitMine Have a Value Mismatch?

After discussing the funding chain and buying retreat, a more fundamental question emerges: Is BitMine's story really over? The current market pricing clearly does not fully understand its structural differences.

Compared to MicroStrategy's path, BitMine chose a completely different approach from the start. MicroStrategy relies heavily on convertible bonds and preferred stock for secondary market fundraising, with annual interest expenses of hundreds of millions of dollars, and its profitability depends on a unilateral bitcoin rally; BitMine, while diluting equity through new share issuance, has almost no interest-bearing debt, and its ETH holdings contribute about 400-500 million USD in staking income annually. This cash flow is relatively rigid and far less correlated with price fluctuations than Strategy's debt costs.

More importantly, this income is not the end. As one of the world's largest institutional ETH holders, BitMine can use staked ETH for restaking (earning an extra 1-2%), operating node infrastructure, locking in fixed income through yield tokenization (such as about 3.5% deterministic yield), or even issuing institutional-grade ETH structured notes—none of which MicroStrategy's BTC holdings can achieve.

However, BitMine (BMNR)'s US stock market cap is currently about 13% lower than its ETH holdings value. In the entire DAT sector, this discount is not the most extreme, but it is clearly below the historical pricing center for similar assets. Bearish sentiment has amplified the visual impact of floating losses, to some extent obscuring the value of income buffering and ecosystem options.

Recent institutional moves seem to have picked up on this deviation. On November 6, ARK Invest increased its holdings by 215,000 shares (8.06 million USD); JPMorgan held 1.97 million shares at the end of Q3. This is not blind bottom-fishing, but based on a judgment of long-term compound growth in the ETH ecosystem. Once Ethereum's price stabilizes or rebounds moderately, the relative stability of income may allow BitMine's mNAV recovery path to be steeper than that of pure leveraged treasuries.

Whether a value mismatch truly exists, the answer is already on the table. The remaining question is only when the market will pay for scarcity. The current discount is both a risk and the starting point of divergence. As Tom Lee said, the pain is short-term and will not change the ETH super cycle. Of course, it may also not change BitMine's core role in this cycle.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Gold declines as positive US data strengthens dollar and reduces expectations for rate cuts

Silicon Valley’s most chaotic split is undoubtedly on its way to the courtroom

Winklevoss Brothers Bitcoin Holdings: The Stunning $1.3 Billion Revelation That Shakes Crypto Markets

Strategic Surge: DDC Enterprise Boldly Purchases 200 Additional Bitcoin, Fortifying Treasury Reserve