Average 401(k) Account Value for Individuals in Their 60s by 2026—Essential Information You Should Be Aware Of

Strategies to Increase Your Retirement Savings in Your 60s

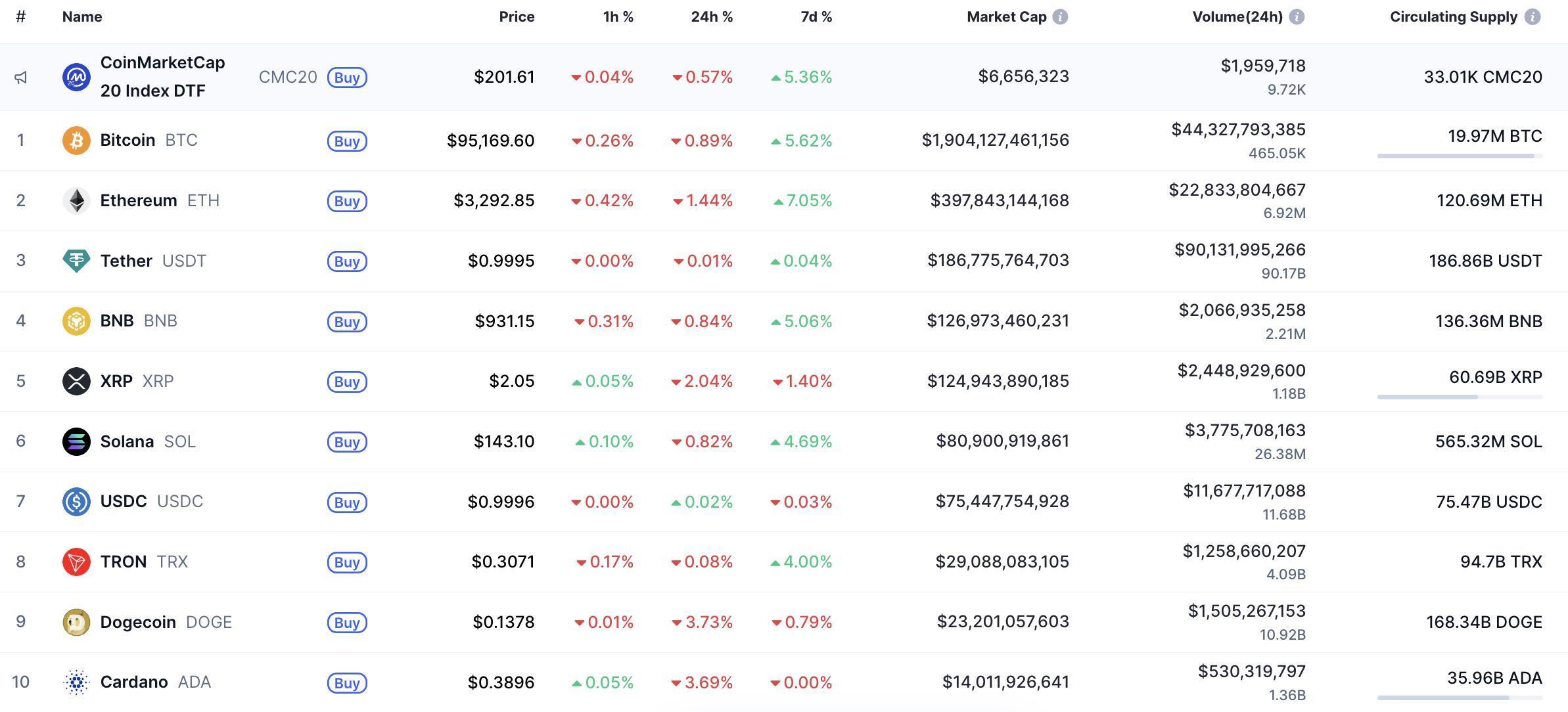

Photo credit: Patricio Nahuelhual / Getty Images

Enhancing your retirement nest egg can be achieved by considering downsizing your home before you retire, maximizing catch-up contributions available in your 60s, and adjusting your investment portfolio to focus on growth opportunities.

Highlights

-

As of June 2025, individuals in their 60s had an average 401(k) balance of $568,040, while the median savings stood at $188,792.

-

The amount you should save for retirement depends on your desired lifestyle and annual spending. A common guideline is to accumulate savings equal to eight times your pre-retirement yearly income by age 60.

Reaching your 60s often brings retirement planning to the forefront. You may wonder how your 401(k) stacks up against others your age and what your actual savings target should be.

While it's natural to compare your progress to your peers, your personal retirement needs will vary based on your intended retirement age and the lifestyle you envision.

Understanding 401(k) Balances in Your 60s

Data from Empower shows that the typical 401(k) balance for people in their 60s was $568,040 as of June 2025. This figure is slightly below the average for those in their 50s, which was $607,055, likely because some in their 60s have already begun withdrawing funds.

It's important to note that averages can be misleading due to a few very high or low balances. The median balance, which better represents the middle ground, was $188,792 in June 2025.

Determining Your Retirement Savings Goal

If you’re concerned about how your retirement savings compare, you’re not alone. A Western & Southern Financial Group survey found that 47% of Baby Boomers—who make up most people in their 60s, as the oldest Gen Xers turn 60 in 2025—lack confidence in their ability to retire comfortably. An additional 11% are uncertain about their retirement prospects.

The same survey revealed that Baby Boomers believe they need about $760,000 to retire comfortably, while Gen Xers estimate they’ll need $1.18 million. These targets are much higher than the average and median 401(k) balances for people in their 60s.

However, your required savings will depend on factors such as your health and the lifestyle you wish to maintain. Rather than focusing solely on averages, it’s wise to assess your unique situation.

One popular rule suggests saving eight times your annual income by age 60. For example, if your salary is $75,000, your goal would be $600,000 in savings by that age.

Alternatively, the 4% rule recommends withdrawing 4% of your retirement savings in your first year of retirement, adjusting for inflation thereafter. This means you should aim to save 25 times your expected annual expenses. So, if you anticipate spending $36,000 per year, you’d need $900,000 set aside.

Additional Income Sources in Retirement

Most retirees don’t rely solely on their 401(k) accounts. Social Security benefits are a major source of income for many, and you might also have IRAs, other investments, or even part-time work to supplement your retirement funds.

The Western & Southern survey found that 90% of Baby Boomers and 71% of Gen Xers expect Social Security to be their main source of retirement income. In contrast, only about half of Millennials and Gen Z (55% and 51%, respectively) anticipate depending primarily on Social Security.

Five Ways to Grow Your Retirement Savings

If your 401(k) balance isn’t where you’d like it to be as you approach retirement, consider these strategies to strengthen your savings in your final working years:

1. Take Advantage of Catch-Up Contributions

For 2025, the standard 401(k) contribution limit is $23,500. However, those aged 60 to 63 can contribute an extra $11,250, bringing the total to $34,750. If you’re 64 or older, your catch-up limit is $7,500, allowing for a maximum contribution of $31,000 in 2025.

2. Maximize Workplace Retirement Benefits

Financial planner Alexa Kane from Pearl Planning advises making full use of your employer’s retirement benefits. If your employer matches contributions, ensure you contribute enough to receive the full match, even if you haven’t done so in the past.

She also recommends automating your savings, as many retirement plans allow you to automatically increase your contributions each year.

3. Adjust Your Investment Mix

When you’re younger, your 401(k) may be heavily invested in stocks for greater growth potential. As retirement nears, it’s common to shift toward a more conservative mix of stocks, bonds, and other assets. If you’re invested in a target-date fund, this transition happens automatically.

If you feel behind on your savings in your 60s, don’t rush to move everything into conservative investments. Maintaining a growth-oriented portfolio for a few more years can help boost your balance. As you get closer to retirement, gradually shifting toward bonds can help protect your savings.

Tip: A financial advisor can help you determine the best asset allocation for your needs and advise you on when to make changes.

4. Downsize Your Living Situation Early

If you’re among the 51% planning to downsize in retirement, consider making this move before you retire. Downsizing now can lower your living expenses by reducing costs such as:

- Property taxes

- Home maintenance and repairs

- Homeowners insurance

- Utility bills

Choosing a new location with access to public transportation can further cut costs by reducing your need for a car. Lowering your expenses allows you to contribute more to tax-advantaged retirement accounts, giving your money more time to grow—especially useful if you’re maximizing catch-up contributions in your early 60s.

5. Consult a Financial Advisor

As you approach retirement, working with a financial advisor can help you clarify your goals and develop a plan to achieve them. Advisors can help you weigh your options and understand the trade-offs involved in different decisions.

For example, some retirees consider moving abroad to benefit from a lower cost of living and more affordable healthcare. However, such a move requires careful planning and knowledge of relevant laws and tax regulations. You’ll still need to file U.S. taxes and understand rules like the Foreign Earned Income Exclusion and Foreign Tax Credit.

A financial advisor can guide you through these complexities and help you choose the retirement path that best fits your resources and priorities.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Kazakhstan liberalizes crypto market through new banking laws

XRP Cyclical Pattern Points to Subsequent Price Expansion

It’s Not Just Crypto Twitter That’s Dead — Experts Say Broader Retail Interest Is Waning

Monero (XMR) Price Analysis for January 16