Why are institutions continuing to raise their holdings of TSMC at this level?

Hello everyone, this is You Dou.

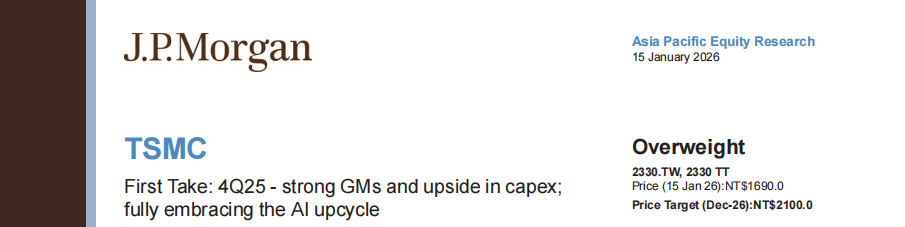

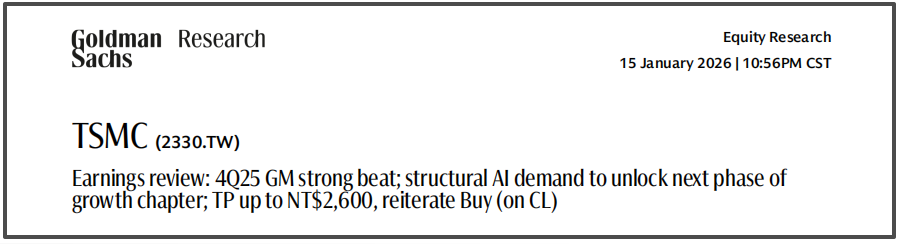

After TSMC released its 4Q25 earnings report, the market responded quickly.

But the real question worth asking is:

Why did institutions choose to continue raising TSMC at this point?

This question is not answered based on intuition.

In this article, I mainly combined the latest research reports released by J.P. Morgan and Goldman Sachs after the earnings report, and from the perspective of institutional models, analyzed why they chose to continue the upward revision at this timing.

Let me give the conclusion first.

This round of upward revision is not because the earnings report looks “good,” but because the original assumptions can no longer stand.

Whether it’s J.P. Morgan or Goldman Sachs, there’s only one thing in common about this move:

It’s not a minor adjustment, but a change in long-term assumptions.

This change is mainly reflected in three aspects.

First Level Reason: AI is No Longer a Marginal Variable

In the past few years, institutional judgment on TSMC’s AI-related revenue was mostly:

Growth is rapid, but it’s still just a subcategory in HPC, with limited impact on long-term models.

After this earnings report, this positioning was completely overturned.

Institutions now generally consider AI accelerator-related revenue as:

the core variable determining advanced process utilization rates

the core variable determining the pace of capital expenditure

and even a variable that determines the overall growth slope of the company

When AI shifts from being “optional” to the “main variable,”

the original growth model naturally needs to be elevated as a whole.

This is not bullish sentiment, but a structural change.

Second Level Reason: 60% Gross Margin Is Becoming the “Norm”

If the revenue side changed the growth slope,

then what changed on the profit side is the valuation anchor itself.

What’s truly important in this earnings report is not that a single quarter’s gross margin exceeded expectations, but that three things happened simultaneously:

4Q25 gross margin stabilized above 60%

1Q26 guidance further raised

Long-term gross margin guidance was clearly raised

The implication behind this is:

Institutions are starting to accept a new premise—

In the coming years, TSMC’s gross margin center may not return to just above 50%.

Once the gross margin center is confirmed to be elevated:

the change in EPS is no longer linear,

but rather the entire profitability range is raised.

This is also why many upward revisions are not achieved by simply increasing the valuation multiple, but by re-pricing EPS.

Third Level Reason: The “Nature” of Capex Has Changed

There has always been controversy in the market over TSMC’s Capex.

But the key to the institutional change in judgment this time is not about how big Capex is, but about why Capex needs to be so large.

This time, institutions characterize Capex as:

not a countercyclical gamble

not a defensive investment

but rather an early layout driven by the long-term certainty of AI demand

In other words:

Capex is no longer regarded as a risk variable, but as the result of growth visibility.

When Capex is understood this way, its meaning for valuation is completely different.

Why Continue Raising “Now” Instead of Earlier or Later?

This is a key question that many people tend to overlook.

Institutions didn’t just realize today that AI is important,

nor did they just now see the tightness in advanced process capacity.

The real trigger is that three things were validated at the same time:

1️⃣ AI demand is no longer just order noise, but a sustainable curve

2️⃣ Gross margin has not been significantly pressured by capacity expansion and overseas deployment

3️⃣ Management has become more decisive regarding medium- and long-term Capex

When all three conditions are met simultaneously,

the original “cautious assumptions” must be revised.

That’s also why the upward revision happened at this point, rather than before the earnings report.

My Understanding

If you only look at the stock price, this upward revision may seem a bit “going with the flow”;

but from the institutional model’s perspective, this is a correction that had to be made.

TSMC is shifting from:

“A highly cyclical manufacturing company”

to:

“The core asset with structural profitability in the AI infrastructure era.”

In this context,

institutions continuing to raise is not aggressive, but lagging.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

TheoriqAI Partners with OpenLedger to Build Accountable, Production-Ready DeFi AI Agents

Betting Shares Decline While NFL Prediction Wagers Rise on Gambling Platforms

Sui Blockchain’s Revolutionary Partnership with LINQ Transforms Crypto Access in Nigeria